Modernising Australia’s human tissue laws

The Attorney-General has announced that he will soon refer the ALRC an inquiry into Australia’s human tissue laws.

It has been almost 50 years since the ALRC completed its 1977 report, Human Tissue Transplants. Significant social, technological, and scientific change in that time means the law has not kept pace, while legislative amendments have produced inconsistencies between state and territory laws. The ALRC’s inquiry will look at how to modernise and harmonise these laws.

The Attorney-General is undertaking a merit-based selection process to identify a suitable Commissioner to lead the inquiry and we look forward to receiving and sharing the Terms of Reference for the inquiry later this year.

ALRC welcomes Tony McAvoy SC

The ALRC is delighted to be joined by Tony McAvoy SC as a Commissioner to lead the ALRC’s Review of the Future Acts Regime.

Tony is a Wirdi man from Central Queensland and is widely recognised as Australia’s most senior First Nations barrister, with over three decades of experience in native title, property, and environmental law.

Through this Inquiry, the ALRC will review the operation of the future acts regime under the Native Title Act 1993 (Cth). We will look at how the future acts regime works now, and how it can be improved to make it work effectively, equally, and fairly.

A one-page Information Sheet and the full Terms of Reference are available on the ALRC website.

Thank you for your submissions

The ALRC sincerely thanks everyone who made a submission in response to the Issues Paper. The experiences and insights shared with us through submissions will help to shape our recommendations for reform.

The ALRC received over 200 submissions and we have begun publishing non-confidential submissions. In recognition of the sensitivities of some submissions and the ALRC’s commitment to a trauma-informed Inquiry process, the ALRC is still processing some submissions for publication. Rather than delay the publication of all submissions, the ALRC will publish submissions in stages.

Please be aware that some of these submissions contain discussion of sexual violence. If you, or someone you know, need help, support services are available (and some are listed immediately below).

Support is available

The ALRC recognises the inherent sensitivities involved in undertaking an inquiry relating to sexual violence. In conducting this Inquiry, the ALRC is employing a trauma-informed and holistic approach to support stakeholders, particularly victim-survivors of sexual violence, and to minimise re-traumatisation.

If you, or someone you know, need help, the following services are available:

- 1800RESPECT call 1800 737 732, text 0458 737 732, https://www.1800respect.org.au/

- Full Stop Australia 1800 385 578 http://www.fullstop.org.au/

- Lifeline 13 11 14 https://www.lifeline.org.au/

- 13YARN 13 92 76 https://www.13yarn.org.au/about-us

- Kids Helpline 1800 55 1800 https://www.kidshelpline.com.au

- Compass (support service for elder abuse) 1800 353 374 https://www.compass.info/

- Rainbow Sexual, Domestic and Family Violence Helpline 1800 497 212 https://fullstop.org.au/get-help/our-services/rainbowviolenceandabusesupport

Further information about support services is available on the ALRC website.

2024 Higinbotham Lecture with ALRC President, Justice Mordy Bromberg

RMIT, 24 October 2024, 5:30 pm

On Thursday 24 October 2024, Justice Bromberg will deliver RMIT’s annual Higinbotham Lecture. The lecture celebrates the legacy of Victorian politician and Chief Justice, George Higinbotham, exploring topical legal issues and the interaction between law and society.

In light of the ALRC’s recent inquiry into Religious Education Institutions and Anti-Discrimination Laws, Justice Bromberg will explore how to approach the delicate task of managing conflicting human rights.

This public lecture is free to attend and registration will remain open via the RMIT website until 21 October 2024.

Wednesday 1 May 2024 at 1.00pm AEST

After more than 20 years of development, the legislative framework for corporations and financial services legislation is no longer fit for purpose. So, what should reform look like?

Join the ALRC for a conversational and interactive analysis of the Final Report in the corporations and financial services legislation Inquiry. The Final Report is the culmination of three years examining the causes and costs of legislative complexity, and contains the ALRC’s 58 recommendations for reform.

Key questions for discussion include:

- why legislative complexity matters;

- how a reformed legislative framework for financial services legislation would reduce complexity; and

- how implementing the ALRC’s reforms would reduce the costs of complexity.

Participants are invited to submit questions for the ALRC panelists both before and during the webinar.

Panel:

- Christopher Ash, Principal Legal Officer, ALRC

- Nicholas Simoes da Silva, Senior Legal Officer, ALRC

- Ellie Filkin, Legal Officer, ALRC

Facilitators:

- June Ahern, Lawyer and Company Law Content Editor, Wolters Kluwer Australia

- Francis Leach, Director of Communications & Media, ALRC

Submit your questions to the panel upon registration or via [email protected]

The Australian Law Reform Commission (ALRC) has recommended legislative reforms to ensure the Australian Government’s policy regarding anti-discrimination laws and religious educational institutions is given legal effect in accordance with Australia’s international legal obligations.

The ALRC’s Report – ‘Maximising the Realisation of Human Rights: Religious Educational Institutions and Anti-Discrimination Laws’, was today tabled in Parliament by the Attorney General and published online.

The implementation of the government’s policy in accordance with the ALRC’s recommendations would mean that under Federal law religious schools are in much the same position as all other schools, except that religious schools would not be prohibited by the Fair Work Act from being able to give preference in employment to a person of the same religion where that is reasonably necessary and proportionate to the school’s objective of building a community of faith.

No school would be permitted to discriminate against students or staff based on those attributes protected by the Sex Discrimination Act (SDA). All schools would continue to have the benefit of those provisions of the SDA which provide that conduct with a disadvantaging effect is not indirectly discriminatory if the conduct is reasonable in the circumstances.*

Currently, under Federal law religious educational institutions are permitted to discriminate against students and staff on certain grounds, including based on sexual orientation, pregnancy, or marital status. However, anti-discrimination laws in many states and both territories already prohibit discrimination against staff and students of religious schools.

The Terms of Reference for this inquiry tasked the ALRC with recommending the legislative reforms required to ensure that the government’s policy when enacted as law, will be consistent with Australia’s international legal obligations.

The ALRC conducted over 130 consultations and received over 400 submissions and 40,000 survey responses. The implementation of the government’s policy in accordance with the ALRC’s recommended reforms will:

- substantially narrow the circumstances in which discrimination by religious educational institutions against their students and staff is permissible at law.

- maximise the enjoyment of human rights and appropriately manage the intersection of rights.

- ensure any restriction of rights is justifiable under international law.

- make federal law more consistent with state and territory laws and the law in comparable overseas.

Quotes from ALRC President, Justice Bromberg: ‘For the law to narrow the circumstances in which it is lawful for religious schools to discriminate against students and staff whilst preserving their capacity to maintain a community of faith, manages the intersection of human rights according to the international law obligations Australia is obliged to respect.’

*For some guidance as to what circumstances may be considered reasonable see 4.162 of the ALRCs Report

Ends

Contact – Francis Leach – 0409 947 180

Download the Final Report

Download the Summary Report

About the Australian Law Reform Commission

The Australian Law Reform Commission (ALRC) is an independent Australian Government agency that provides recommendations for law reform to Government on issues referred to it by the Attorney-General of Australia.

|

|

|

|

Media contact: |

Francis Leach, Media and Communications Director [email protected], 0409 947 180 |

Over the past few years, the ALRC used pioneering data collection and analysis to scrutinise corporations and financial services legislation. Using legislative data, the ALRC was able to show just how complex corporations and financial services legislation is. The ALRC also used that data when developing reforms.

Over the past few years, the ALRC used pioneering data collection and analysis to scrutinise corporations and financial services legislation. Using legislative data, the ALRC was able to show just how complex corporations and financial services legislation is. The ALRC also used that data when developing reforms.

This article aims to answer some of the (hypothetically) frequently asked questions about the Legislative Data Framework recommended by the ALRC (Recommendation 58). The Legislative Data Framework would be a publicly available data framework for monitoring the development of corporations and financial services legislation. As outlined below, it would be a useful tool for several different users of the legislation.

This is the sixth (and final) in a series of short pieces following the release of the ALRC’s Final Report relating to the legislative framework for corporations and financial services regulation.

What is legislative data?

What is legislative data?

By treating legislation as data (or a dataset), a wide range of data points can be generated. These include, for example, page length, word length, the number of chapters, parts, or sections, the number of defined terms, and the frequency with which defined terms are used. This data can then be analysed to generate novel insights into the law, as the ALRC has done when investigating the complexity of corporations and financial services legislation. The use of legislative data underscores the ALRC’s commitment to evidence-based law reform.

The ALRC’s DataHub contains the data sets used by the ALRC and several illustrations of how legislative data can be used.

What is the Legislative Data Framework?

The Legislative Data Framework would provide a publicly available resource for users of corporations and financial services legislation.

The Legislative Data Framework has three main purposes:

- to provide resources that help stakeholders navigate and understand the legislation;

- to help government administer and reform the legislation; and

- to allow legislation to be monitored over time and for stakeholders to hold government accountable for the legislation’s development over time.

Recommendation 58 sets out the types of legislative data that the ALRC recommends that the framework should track. This includes, for example:

- How many pieces of principal primary and delegated legislation are currently in force?

- How many are enacted each year?

- How long are they (how many pages and words)?

- How many powers to make regulations (and other legislative instruments) are in force?

- How many of those powers are enacted each year?

- How many times have those powers been exercised?

- How many notional amendments are in force and enacted annually?

- Which pieces of legislation do those notional amendments affect?

For more information on the legislative data framework, see Chapter 10 of the Final Report.

How has the ALRC used legislative data in this Inquiry?

The ALRC has used computational methods to analyse over 53GB of textual data. This is the equivalent of over 10 million pages of documents, including: more than 13,000 Acts, 89,000 legislative instruments, more than 35,000 legislation compilations, 101,000 court judgments, and 200 regulatory guides.

The ALRC wrote a number of computer programs using ‘R’ programming language to ‘scrape’ the HTML of legislation and metadata legislation from the Federal Register of Legislation website. This data was then computationally analysed to help the ALRC measure and understand the breadth of the legislative complexity in the financial services legislative framework.

For more information on the methodology used in this Inquiry, see Interim Report A.

How does the ALRC see the Legislative Data Framework being used?

The Terms of Reference for the Inquiry asked the ALRC to consider ‘how legislative complexity can be appropriately managed over time’. The Legislative Data Framework would help do this.

In particular, it would be used to:

- support government and regulators to make it easier to produce higher quality legislation, and to perform their regulatory stewardship roles; and

- promote accountability by providing the basis for accountability dashboards that track changes in the volume of legislation, regulatory guidance, notional amendments, unused legislative powers, offences, and other penalties.

The ALRC suggests that the Legislative Data Framework should be used alongside a legislative complexity framework. Currently, there is very little research into legislative complexity in Australia. This legislative complexity framework would seek to fill that gap.

The legislative complexity framework would provide a way to track how particular legislative features make legislation more or less complex over time. For more information on the legislative complexity framework, see Chapter 10 of the Final Report.

What is currently being done with data and legislation?

Legislative data is being used for more than just corporations and financial services legislation.

The Australian Government recently completed a Review of the Migration System. In the Review, the legislative and policy complexity of migration law was highlighted through the use of data and visualisations.

Similarly, Associate Professor Crawford and others used data collected from the Federal Register of Legislation to measure complexity across several federal Acts.

The NSW Government Legislation Twin uses data so that stakeholders can gain a better understanding of the interconnections between NSW legislation, other legal instruments, and government agencies and ministers.

How resource-intensive would a Legislative Data Framework be?

The majority of the ALRC’s data collection and publication was performed by the equivalent of less than one full-time staff member, with modest computing resources. The ALRC’s experience suggests that the Legislative Data Framework would not require considerable resources.

What could the legislative data framework be used for in the future?

There are many potential future uses for the Legislative Data Framework. The ALRC has discussed how the framework could facilitate the development of regulatory technology (commonly referred to as ‘RegTech’) and other technological solutions to aid compliance.

In the future, the data framework could be extended to obtain more granular data, which would provide specific insights on particular aspects of legislation. For an example of how such granular data could be used, see Chapter 3 of Interim Report A.

The data framework could also be extended to cover all Commonwealth legislation. This would have benefits for everyone who uses Commonwealth legislation, as well as those who are involved in legislative scrutiny and maintenance.

This article answers some of the (hypothetically) frequently asked questions about the Financial Services Law Schedule (the ‘FSL Schedule’) recommended by the ALRC. Implementing two of the ALRC’s recommendations would produce the FSL Schedule:

- creating the Financial Services Law by restructuring and reframing the financial services provisions within Chapter 7 of the Corporations Act 2001 (Cth) (‘Corporations Act’) and Part 2 Div 2 of the Australian Securities and Investments Commission Act 2001 (Cth) (‘ASIC Act’) (Recommendation 41); and

- enacting the Financial Services Law as Sch 1 to the Corporations Act (Recommendation 42).

This is the fifth in a series of short pieces following the release of the ALRC’s Final Report relating to the legislative framework for corporations and financial services regulation.

What is the FSL Schedule?

The FSL Schedule would contain the key provisions relating to the regulation of financial products and financial services. It would be a clearly identifiable body of primary legislation that would be more coherently structured and easier to navigate than existing legislation.

The FSL Schedule would replace most of Chapter 7 of the Corporations Act and the entire Part 2 Div 2 of the ASIC Act, thereby reducing the number of places users need to look to find the law.

What would the FSL Schedule contain?

The FSL Schedule would contain the most important regulatory provisions, such as core obligations, core prohibitions, offence provisions, rights, remedies, and definitions.

The FSL Schedule would comprise three elements:

- all of the key financial services-related provisions that are currently found in Chapter 7 of the Corporations Act and Part 2 Div 2 of the ASIC Act; and

- objects clauses which would identify the fundamental norms of behaviour underpinning the legislation; and

- a list of defined terms.

The provisions of the FSL Schedule would be structured and framed in a way that would make it as easy to navigate and understand as possible. For more detail about how this could be done, see Chapter 5 of the Final Report.

Why did the ALRC recommend a schedule?

As discussed in Interim Report C, a schedule would allow the greatest flexibility to restructure and reframe the existing legislation while causing the least amount of disruption to other parts of the Corporations Act and ASIC Act.

In addition, the ALRC recommends that the Financial Services Law be contained in a schedule because:

- a schedule can be used to create a clearer legislative ‘identity’ for the regulation of financial services and to highlight common themes that traverse several chapters;

- it would be easier to facilitate integration of Part 2 Div 2 of the ASIC Act because all levels of the macrostructure (such as chapters and parts) could be used;

- retaining the substance of Chapter 7 in a schedule to the Corporations Act would enable existing linkages with other parts of the Act to be maintained more easily; and

- provision numbering in the schedule could ‘start afresh’, whereas any restructuring of the provisions of Chapter 7 of the Corporations Act would require renumbering.

What did stakeholders say about the idea?

A number of stakeholders provided submissions in response Interim Report C, where the ALRC first suggested the FSL Schedule. Stakeholders were generally supportive of the proposal.

Some stakeholders commented on the structure of the proposed FSL Schedule, and others made suggestions about other licensing regimes that could be included in the Schedule.

Several stakeholders expressed a preference for the Financial Services Law to be enacted as a standalone Act, but in light of existing constitutional constraints were supportive of the proposed schedule.

For further discussion, see the ALRC’s background paper on ‘Reflecting on Reforms III — Submissions to Interim Report C’.

Is there a risk that people will think the provisions in the FSL Schedule are less important than the provisions in the body of the Corporations Act?

This was a concern that some stakeholders raised with the ALRC. At least one stakeholder raised a concern that putting the Financial Services Law in a schedule ‘may lead to a perception that financial services regulation is not deserving of a prominent place in our Australian laws’.

However, the FSL Schedule would not be the first instance of a regulatory scheme being contained within a schedule to an Act. Other examples include:

- The Australian Consumer Law, in Sch 1 to the Competition and Consumer Act 2010 (Cth). The location of the Australian Consumer Law in a schedule was driven by the legislation’s constitutional basis, like the FSL Schedule.

- The Criminal Code in a schedule to the Criminal Code Act 1995 (Cth).

- The National Credit Code in which is Sch 1 to the National Consumer Credit Protection Act 2009 (Cth) (‘NCCP Act’).

- The Insolvency Practice Schedule (Corporations) and Insolvency Practice Schedule (Bankruptcy) contained in, respectively, Sch 2 to the Corporations Act and Sch 2 to the Bankruptcy Act 1966 (Cth).

As discussed in Interim Report C, experience with the Australian Consumer Law suggests that its location in a schedule has improved, rather than detracted from, public awareness of the legislation.

What alternatives did the ALRC consider?

During the Inquiry, the ALRC canvassed several alternatives, such as:

- enacting the Financial Services Law as a standalone Act;

- consolidating similar and overlapping regulatory regimes currently spread across different pieces of corporations and financial services legislation (for example, the Corporations Act, NCCP Act 2009 (Cth), ASIC Act, and Superannuation Industry (Supervision) Act 1993 (Cth)); and

- inserting the Financial Services Law as a new chapter within the Corporations Act.

For discussion of these alternatives, see Chapter 8 of the Final Report.

Why did the ALRC not recommend a standalone Act?

The ALRC has not recommended a standalone Act or consolidation of regulatory regimes for two main reasons. First, doing so may go beyond the Terms of Reference for the Inquiry, including because it may involve questions of policy.

Throughout the Inquiry, several stakeholders suggested there should be a standalone Act relating to financial services. In part, these suggestions stem from the perception that Chapter 7 of the Corporations Act is like an ‘Act within an Act’ in terms of its length and scope (see Chapter 8 of Interim Report C for further discussion). Some stakeholders would also prefer financial services provisions to be in a standalone Act to emphasise how important financial services regulation is within Australian law.

Second, enacting one or more standalone Acts would appear to be possible only by reforming the existing constitutional basis for the Corporations Act. In brief, the current referral of matters from the States to the Commonwealth would not empower the Commonwealth to enact other (standalone) primary legislation relating to the regulation of corporations and financial services.

Nevertheless, should a standalone Act or consolidation of regulatory regimes be considered, the ALRC’s recommendations could provide a useful starting point for that legislation.

For discussion of the constitutional underpinnings of the corporations and financial services legislation, see the ALRC’s background paper on ‘Historical Legislative Developments’ and Chapter 5 of the Final Report.

Why did the ALRC not recommend a new chapter of the Corporations Act?

The ALRC has not recommended that the Financial Services Law be enacted as a new chapter to the Corporations Act (or, alternatively, the ASIC Act) for two key reasons. First, there is no obvious ‘home’ for the Financial Services Law within either Act. Second, a schedule (as opposed to a new chapter) can be used to create a clearer legislative ‘identity’ for the regulation financial services and to highlight common themes that traverse several chapters.

Is it pronounced ‘shedule’ or ‘skedule’?

This question prompts heated debate on the internet (and even divides some of the ALRC team), so we’ll stay out of this one.

Throughout the Corporations and Financial Services Legislation Inquiry, stakeholders emphasised the importance of staging the implementation of reforms and managing transition costs. This article explains the ALRC’s suggested approach for implementing the reformed legislative framework for financial services.

This is the fourth in a series of short pieces following the release of the ALRC’s Final Report relating to the legislative framework for corporations and financial services regulation. In an earlier article, we outlined the reformed framework and explained how users would navigate it.

Why devote a whole chapter of the Final Report to Implementation?

Implementing reform comes with challenges and risks, such as transition costs and a risk that the job is left only half done. Chapter 7 of the Final Report details the ALRC’s approach to implementation and explains how the reformed legislative framework could be implemented in a logical, staged way so as to realise the benefits of reform as early as possible, minimise transition costs, and reduce the risk of it being left incomplete.

In summary, the ALRC’s suggested approach has two main elements:

- a Reform Roadmap (which sets out six Reform Pillars to guide implementation); and

- Steps to Implementation (which detail how each Reform Pillar should be approached).

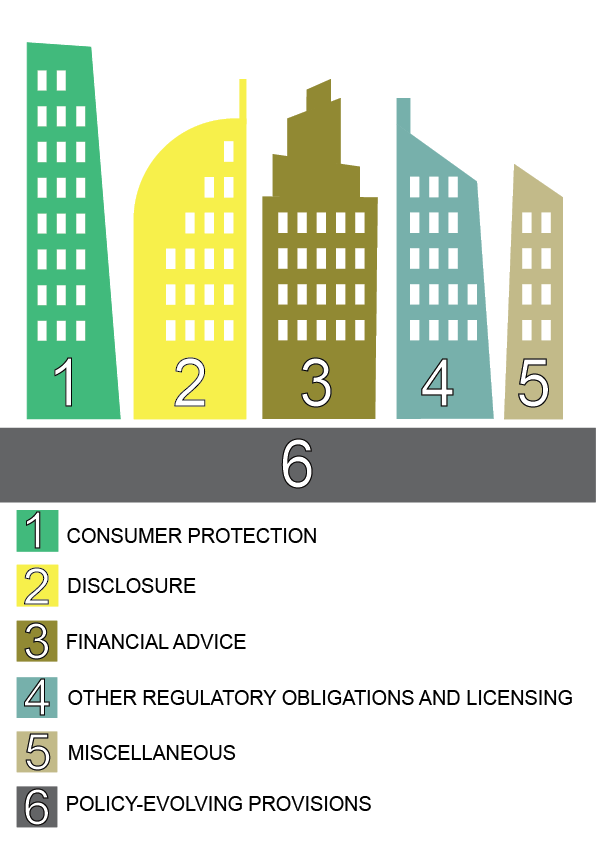

The Reform Roadmap and the Six Reform Pillars

The ALRC’s approach to implementing the reformed legislative framework is built on six Reform Pillars, shown in the following diagram:

The order of the Pillars is important. The Reform Roadmap is structured to realise the benefits of reform as early as possible.

- Pillar One (Consumer Protection) lays the foundation for future reforms. It does this by ensuring the legislation better communicates fundamental norms and frames the more specific obligations in later pillars.

- Pillar Two (Disclosure) would have a significant impact on reducing unnecessary complexity, with benefits for regulated persons, consumers, and investors.

- Pillar Three (Financial Advice) would bring together and consolidate the currently disparate provisions relating to financial advice, helping to reduce the costs of advice, support advisers to understand their obligations, and promote higher quality advice.

- Pillar Four (Other Regulatory Obligations and Licensing) would simplify the myriad regulatory obligations of financial services providers, and would complete the process of establishing a more navigable and comprehensible legislative framework.

- Pillar Five (Miscellaneous) would deal with reforms that are not captured by other pillars.

- Pillar Six (Policy-Evolving Provisions) provides a means of accommodating policy developments and policy reform alongside creation of the reformed legislative framework.

The ALRC recommends that the Reform Roadmap and implementation process be overseen by a specifically resourced taskforce (or taskforces) dedicated to that task (Recommendation 54). Taskforces are often used to implement reforms, drawing on expertise both within and outside government. Utilising a taskforce to implement reforms is an important way of minimising the challenges that confront any reform project.

Further detail about each of the Reform Pillars and taskforces is contained in Chapter 7 of the Final Report.

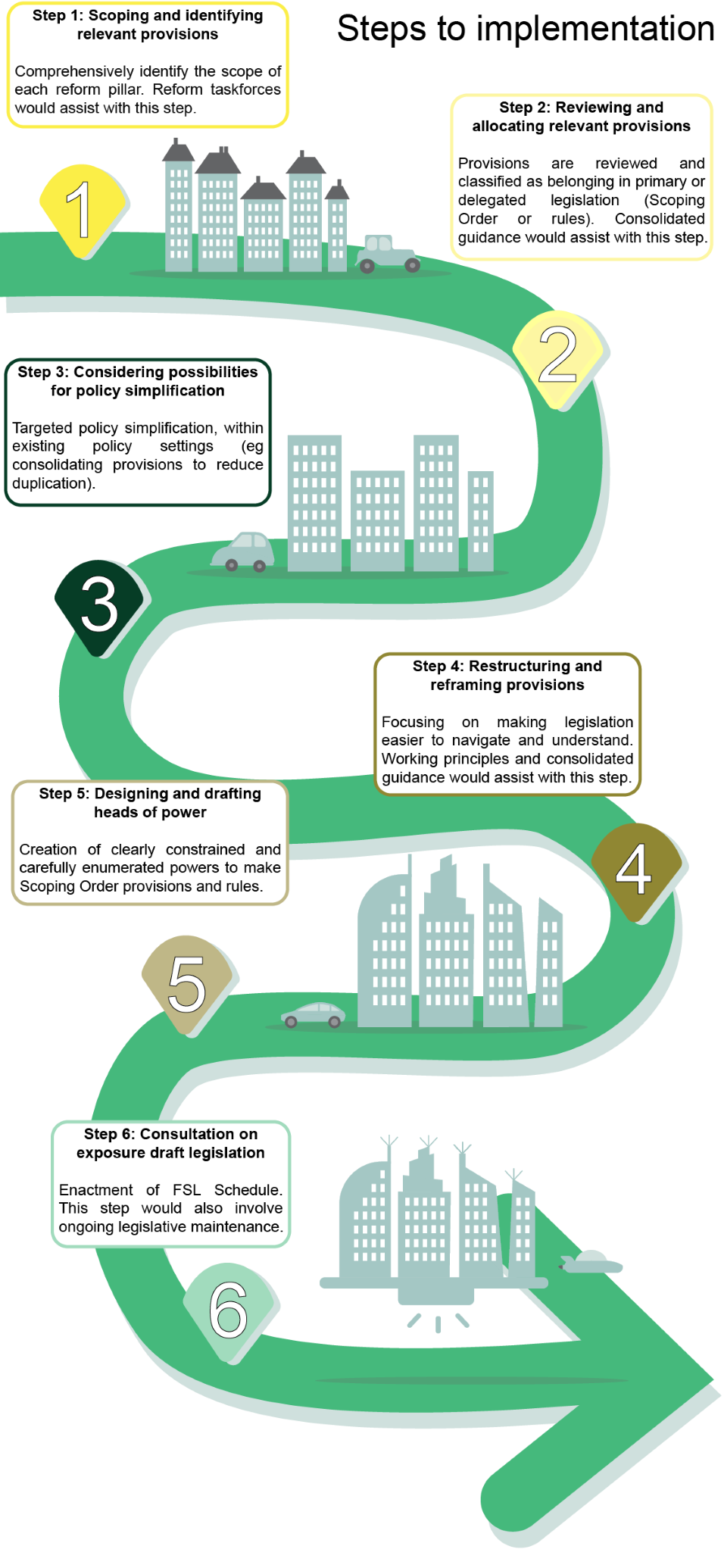

Steps to Implementation

Each Reform Pillar in the Roadmap would be implemented by following the six steps set out below:

In summary, the Steps to Implementation would involve:

- developing a clear understanding of the existing legislative framework and the design of the reformed legislative framework (Steps 1 and 2);

- looking at the bigger picture, to identify instances where targeted policy simplification could complement technical reforms to reduce legislative complexity (Step 3);

- applying best-practice principles of legislative design when preparing the legislation that implements the reformed legislative framework (Steps 4 and 5); and

- ensuring the reformed legislative framework is maintained into the future (Step 6), which should include periodic post-enactment review (Recommendation 55).

Chapter 7 of the Final Report contains further detail about the implementation process and explains the importance of ongoing legislative maintenance.

The ALRC used a number of analogies during the Corporations and Financial Services Legislation Inquiry to help explain our discoveries and conceptualise our insights about legislative complexity. We likened the law to a house, a cupboard, Russian dolls, and even outer space. Looking back, it often felt like we were on an archaeological dig, excavating layers of complexity when trying to understand the legislation we were meant to reform.

This infographic by ALRC Legal Officer/artist, Ellie Filkin, explores what that three-year archaeological dig looked like for the ALRC. It might resonate with some users of corporations and financial services legislation.

This is the third in a series of short pieces following the release of the ALRC’s Final Report relating to the legislative framework for corporations and financial services regulation.

The Hon. Marcia Neave AO, and Judge Liesl Kudelka of the South Australian District Court will lead the ALRC’s Justice’s Response to Sexual Violence inquiry which was announced this week by Attorney General Mark Dreyfus KC MP. Both appointees bring with them deep expertise and experience of the justice system, particularly as it relates to issues involving sexual violence.

Hon. Marcia Neave AO

Marcia Neave has had a distinguished career having served as a judge, commissioner, law reformer, public policy maker, and academic. After nine years on the Supreme Court of Victoria, Court of Appeals Division, she was appointed to the role of Commissioner of the Victorian Royal Commission into Family Violence. In 2021 she was named as President and Commissioner of the Commission of Inquiry into the Tasmanian Government’s Responses to Child Sexual Abuse in Institutional Settings.

She was the inaugural Chair of the Victorian Law Reform Commission which in 2004 recommended substantial changes to criminal laws and procedures dealing with sexual assault. She has also been Professor at ANU, Adelaide, and Monash Universities.

Judge Liesl Kudelka

Judge Kudelka was appointed as a Judge of the District Court of South Australia in October 2017. She has 25 years of experience in the criminal jurisdiction as a judge, barrister, and prosecutor.

In 2020, Judge Kudelka prepared a detailed written proposal for a pilot Priority Programme in the District Court of South Australia to improve justice responses for alleged victims of sexual assault and domestic violence by implementing new processes to reduce delays in proceedings. Judge Kudelka implemented the programme and has been managing it since May 2021.

Amongst her many professional achievements, Judge Kudelka was a prosecutor in the Office of The Director of Public Prosecutions in South Australia, as well as working on the discussion paper ‘Review of South Australian Rape and Sexual Assault Law’ in 2006. She also acted as Counsel Assisting ‘the Children in State Care Commission of Inquiry: Allegations of Sexual Abuse & Death from Criminal Conduct’ (SA) in 2007 – 2008.

Marcia Neave AO (left) and Judge Liesl Kudelka (right) will lead the inquiry for the ALRC.

Inquiry into Justice Responses to Sexual Violence

The ALRC will take a take a trauma-informed, holistic, whole-of-systems, and transformative approach to its inquiry, whilst considering matters raised for reform and detailed in prior reports and inquiries.

The inquiry will consult with relevant stakeholders across Australia, including but not limited to:

- people who have experienced sexual violence.

- people and organisations representing population cohorts that are overrepresented in sexual violence statistics.

- state and territory government and law enforcement agencies.

- policy and research organisations.

- community service providers; and

- the legal profession including prosecution and defence lawyers.

The inquiry is due to provide its final report to the Attorney-General in January of 2025.

Further information on the work of the ALRC: https://www.alrc.gov.au/

The existing legislative framework for financial services is unnecessarily complex and difficult to use. So how should it be improved?

This article briefly explores the reformed legislative framework for financial services legislation recommended by the ALRC in the Final Report of the Corporations and Financial Services Legislation Inquiry. It also illustrates the benefits of the reformed legislative framework by showing how it would be much simpler to navigate than the existing legislative framework.

This is the second article in a series of short pieces following the release of the ALRC’s Final Report. Revisit the first article here.

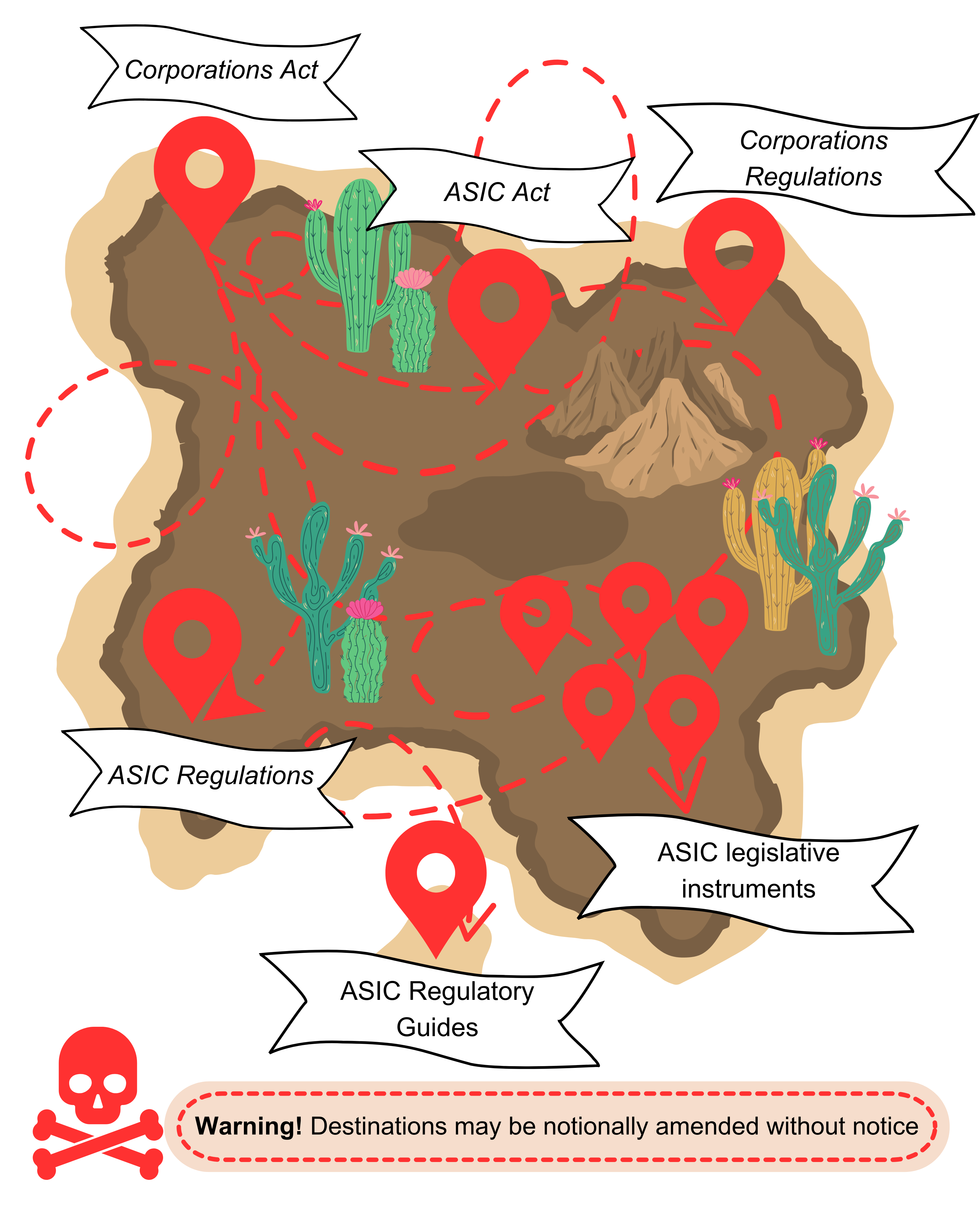

The existing legislative framework

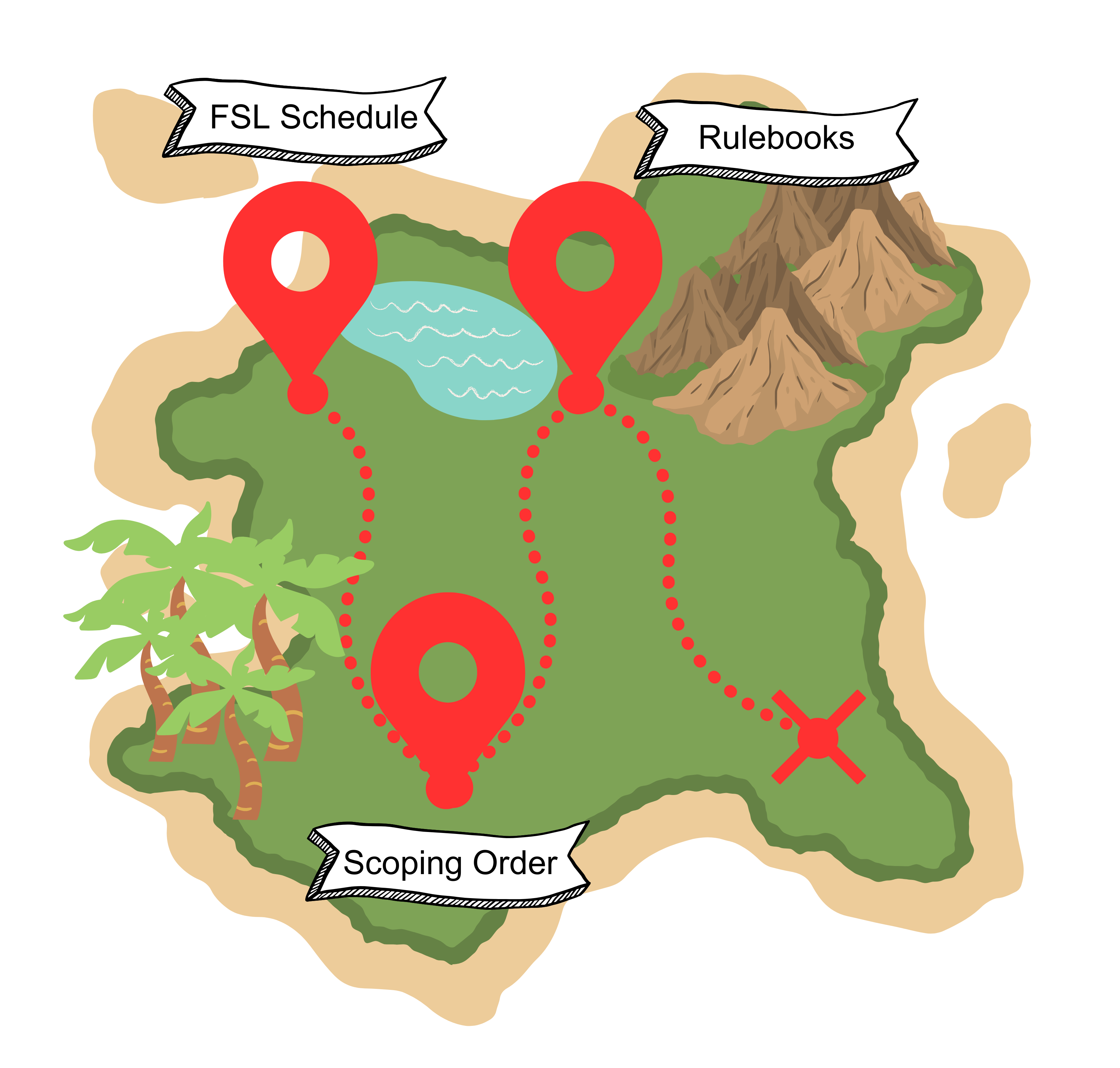

Currently, if a person wants to use financial services legislation, they must wade their way through voluminous Acts, regulations, legislative instruments, and guides, with little indication as to what they can expect to find and where. Navigating the existing legislative framework is a bit like using a treasure map that has many paths, but no clear destination:

The reformed legislative framework

If implemented, the ALRC’s recommendations would transform the existing legislative framework into the reformed legislative framework.

The reformed legislative framework is intended to be clear, user-friendly, and easy to navigate:

- Users would start with the Financial Services Law Schedule (‘FSL Schedule’), where they would find key provisions including important obligations, prohibitions, offences, and penalties. The FSL Schedule would be enacted by Parliament, reflecting the significance of its contents.

- Users would then move to the single, consolidated Scoping Order. In the Scoping Order, users would find provisions that set the scope of the regulatory framework, such as exclusions.

- Users would then move to thematic Rulebooks, where they would find prescriptive detail about how to comply with obligations in the FSL Schedule.

Compared to the existing legislative framework, users would end their journey (where ‘x’ marks the spot) having followed a clearly defined path and without the need to consider whether any part of the law has been notionally amended by another piece legislation. Because the reformed legislative framework would be simple to navigate, it would also be easier for users to develop a clear understanding of their obligations or rights.

Each element of the reformed legislative framework is based on working principles for legislative design set out in the Final Report, all of which help to make the framework easier to navigate and understand:

Each element of the reformed legislative framework is based on working principles for legislative design set out in the Final Report, all of which help to make the framework easier to navigate and understand:

- coherence;

- grouping thematically related provisions;

- intuitive flow;

- prioritisation;

- succinctness;

- consolidating similar provisions; and

- mental models.

Though directed at the legislation that governs financial services, the principles that underpin the reformed legislative framework could be applied to other legislation (especially complex legislation).

For more information, see the Final Report:

- Chapter 3 gives an overview of the reformed legislative framework;

- Chapter 4 discusses the ALRC’s working principles for legislative design that underpin the reformed legislative framework; and

- Chapters 5 and 6 set out the elements of the reformed legislative framework in more detail, discussing how the primary legislation should be restructured and reframed (Chapter 5) and make better use of the legislative hierarchy (Chapter 6).

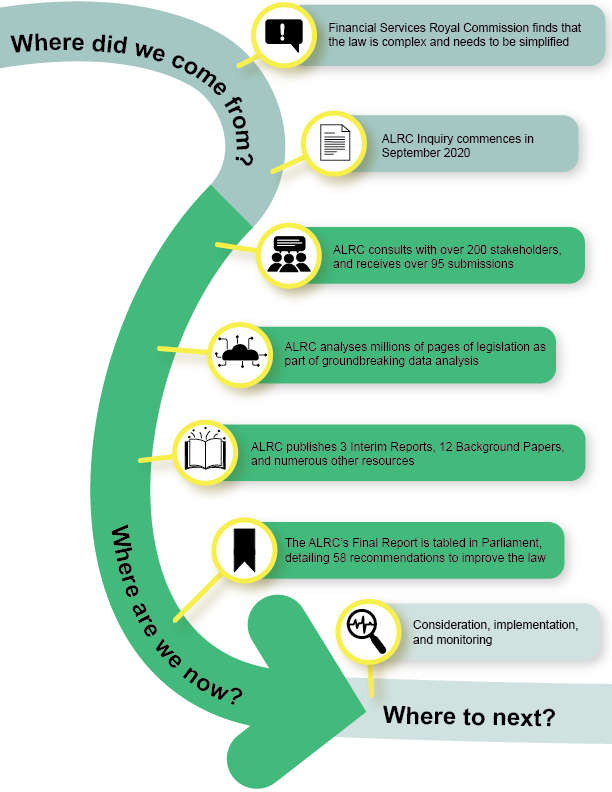

Last week, the Final Report of the ALRC’s Corporations and Financial Services Inquiry was published. The Final Report laid out the results of three years’ work examining why the law is so complex and setting out how it should be reformed. In this article, we describe the ALRC’s journey from the Inquiry’s genesis through to next steps.

This is the first in a series of short articles following the release of the Final Report. Each piece aims to give a simple overview of the ALRC’s recommendations and important themes from the inquiry.

Where did we come from?

In 2019, the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (also known as the Hayne Royal Commission) found that corporations and financial services legislation is overly complex and in need of simplification. In particular, the Royal Commission found that financial services legislation fails to communicate the fundamental norms of behaviour that it promotes.

Against this background, the Australian Government gave the ALRC Terms of Reference, which tasked the ALRC with making financial services and corporations legislation clearer and more understandable.

The ALRC’s analysis confirms that corporations and financial services legislation remains unnecessarily complex. The main sources of unnecessary complexity include:

- an incoherent legislative hierarchy;

- poorly designed primary and delegated legislation;

- issues with law-making processes and legislative maintenance;

- extensive use of notional amendments; and

- proliferating powers and instruments creating a legislative maze.

See Chapter 2 of the Final Report for more details.

Where are we now?

The ALRC consulted with a wide variety of stakeholders, including regulators, government departments, academics, legal professionals, and industry representative bodies. Stakeholders were given the opportunity to provide feedback and formal submissions in response to the ALRC’s preliminary proposals throughout the Inquiry. Stakeholders almost universally agreed with the ALRC that the existing legislation is complex and that it should be simplified.

The ALRC also produced groundbreaking new empirical data analysis, providing fresh insights into the causes and consequences of legislative complexity. The ALRC’s empirical analysis confirmed stakeholders’ anecdotal experience of complexity. Further detail about the ALRC’s data analysis is available on the ALRC Data Hub.

Throughout the Inquiry, the ALRC published 12 Background Papers, and three Interim Reports.

The ALRC has now published its Final Report, which contains 58 recommendations for reform (23 of these recommendations were made in the three Interim Reports). These recommendations aim to simplify and rationalise corporations and financial services legislation, making it easier to use and understand.

Where to next?

Now that the Final Report has been published, the Australian Government will consider which of the ALRC’s recommendations should be implemented. Several recommendations made by the ALRC in Interim Reports A and B have already been implemented.

Chapter 7 of the Final Report sets out a staged process for implementing many of the recommendations. This staged process categorises the recommendations into six ‘Pillars’. See Chapter 7 of the Final Report for more details.

The ALRC has also recommended several measures to ensure that the recommendations have an enduring effect into the future. This includes the creation of guidance for legislative drafting, and a legislative data framework to monitor the development of corporations and financial services legislation.