Wednesday 1 May 2024 at 1.00pm AEST

After more than 20 years of development, the legislative framework for corporations and financial services legislation is no longer fit for purpose. So, what should reform look like?

Join the ALRC for a conversational and interactive analysis of the Final Report in the corporations and financial services legislation Inquiry. The Final Report is the culmination of three years examining the causes and costs of legislative complexity, and contains the ALRC’s 58 recommendations for reform.

Key questions for discussion include:

- why legislative complexity matters;

- how a reformed legislative framework for financial services legislation would reduce complexity; and

- how implementing the ALRC’s reforms would reduce the costs of complexity.

Participants are invited to submit questions for the ALRC panelists both before and during the webinar.

Panel:

- Christopher Ash, Principal Legal Officer, ALRC

- Nicholas Simoes da Silva, Senior Legal Officer, ALRC

- Ellie Filkin, Legal Officer, ALRC

Facilitators:

- June Ahern, Lawyer and Company Law Content Editor, Wolters Kluwer Australia

- Francis Leach, Director of Communications & Media, ALRC

Submit your questions to the panel upon registration or via financial.services@alrc.gov.au

Over the past few years, the ALRC used pioneering data collection and analysis to scrutinise corporations and financial services legislation. Using legislative data, the ALRC was able to show just how complex corporations and financial services legislation is. The ALRC also used that data when developing reforms.

Over the past few years, the ALRC used pioneering data collection and analysis to scrutinise corporations and financial services legislation. Using legislative data, the ALRC was able to show just how complex corporations and financial services legislation is. The ALRC also used that data when developing reforms.

This article aims to answer some of the (hypothetically) frequently asked questions about the Legislative Data Framework recommended by the ALRC (Recommendation 58). The Legislative Data Framework would be a publicly available data framework for monitoring the development of corporations and financial services legislation. As outlined below, it would be a useful tool for several different users of the legislation.

This is the sixth (and final) in a series of short pieces following the release of the ALRC’s Final Report relating to the legislative framework for corporations and financial services regulation.

What is legislative data?

What is legislative data?

By treating legislation as data (or a dataset), a wide range of data points can be generated. These include, for example, page length, word length, the number of chapters, parts, or sections, the number of defined terms, and the frequency with which defined terms are used. This data can then be analysed to generate novel insights into the law, as the ALRC has done when investigating the complexity of corporations and financial services legislation. The use of legislative data underscores the ALRC’s commitment to evidence-based law reform.

The ALRC’s DataHub contains the data sets used by the ALRC and several illustrations of how legislative data can be used.

What is the Legislative Data Framework?

The Legislative Data Framework would provide a publicly available resource for users of corporations and financial services legislation.

The Legislative Data Framework has three main purposes:

- to provide resources that help stakeholders navigate and understand the legislation;

- to help government administer and reform the legislation; and

- to allow legislation to be monitored over time and for stakeholders to hold government accountable for the legislation’s development over time.

Recommendation 58 sets out the types of legislative data that the ALRC recommends that the framework should track. This includes, for example:

- How many pieces of principal primary and delegated legislation are currently in force?

- How many are enacted each year?

- How long are they (how many pages and words)?

- How many powers to make regulations (and other legislative instruments) are in force?

- How many of those powers are enacted each year?

- How many times have those powers been exercised?

- How many notional amendments are in force and enacted annually?

- Which pieces of legislation do those notional amendments affect?

For more information on the legislative data framework, see Chapter 10 of the Final Report.

How has the ALRC used legislative data in this Inquiry?

The ALRC has used computational methods to analyse over 53GB of textual data. This is the equivalent of over 10 million pages of documents, including: more than 13,000 Acts, 89,000 legislative instruments, more than 35,000 legislation compilations, 101,000 court judgments, and 200 regulatory guides.

The ALRC wrote a number of computer programs using ‘R’ programming language to ‘scrape’ the HTML of legislation and metadata legislation from the Federal Register of Legislation website. This data was then computationally analysed to help the ALRC measure and understand the breadth of the legislative complexity in the financial services legislative framework.

For more information on the methodology used in this Inquiry, see Interim Report A.

How does the ALRC see the Legislative Data Framework being used?

The Terms of Reference for the Inquiry asked the ALRC to consider ‘how legislative complexity can be appropriately managed over time’. The Legislative Data Framework would help do this.

In particular, it would be used to:

- support government and regulators to make it easier to produce higher quality legislation, and to perform their regulatory stewardship roles; and

- promote accountability by providing the basis for accountability dashboards that track changes in the volume of legislation, regulatory guidance, notional amendments, unused legislative powers, offences, and other penalties.

The ALRC suggests that the Legislative Data Framework should be used alongside a legislative complexity framework. Currently, there is very little research into legislative complexity in Australia. This legislative complexity framework would seek to fill that gap.

The legislative complexity framework would provide a way to track how particular legislative features make legislation more or less complex over time. For more information on the legislative complexity framework, see Chapter 10 of the Final Report.

What is currently being done with data and legislation?

Legislative data is being used for more than just corporations and financial services legislation.

The Australian Government recently completed a Review of the Migration System. In the Review, the legislative and policy complexity of migration law was highlighted through the use of data and visualisations.

Similarly, Associate Professor Crawford and others used data collected from the Federal Register of Legislation to measure complexity across several federal Acts.

The NSW Government Legislation Twin uses data so that stakeholders can gain a better understanding of the interconnections between NSW legislation, other legal instruments, and government agencies and ministers.

How resource-intensive would a Legislative Data Framework be?

The majority of the ALRC’s data collection and publication was performed by the equivalent of less than one full-time staff member, with modest computing resources. The ALRC’s experience suggests that the Legislative Data Framework would not require considerable resources.

What could the legislative data framework be used for in the future?

There are many potential future uses for the Legislative Data Framework. The ALRC has discussed how the framework could facilitate the development of regulatory technology (commonly referred to as ‘RegTech’) and other technological solutions to aid compliance.

In the future, the data framework could be extended to obtain more granular data, which would provide specific insights on particular aspects of legislation. For an example of how such granular data could be used, see Chapter 3 of Interim Report A.

The data framework could also be extended to cover all Commonwealth legislation. This would have benefits for everyone who uses Commonwealth legislation, as well as those who are involved in legislative scrutiny and maintenance.

This article answers some of the (hypothetically) frequently asked questions about the Financial Services Law Schedule (the ‘FSL Schedule’) recommended by the ALRC. Implementing two of the ALRC’s recommendations would produce the FSL Schedule:

- creating the Financial Services Law by restructuring and reframing the financial services provisions within Chapter 7 of the Corporations Act 2001 (Cth) (‘Corporations Act’) and Part 2 Div 2 of the Australian Securities and Investments Commission Act 2001 (Cth) (‘ASIC Act’) (Recommendation 41); and

- enacting the Financial Services Law as Sch 1 to the Corporations Act (Recommendation 42).

This is the fifth in a series of short pieces following the release of the ALRC’s Final Report relating to the legislative framework for corporations and financial services regulation.

What is the FSL Schedule?

The FSL Schedule would contain the key provisions relating to the regulation of financial products and financial services. It would be a clearly identifiable body of primary legislation that would be more coherently structured and easier to navigate than existing legislation.

The FSL Schedule would replace most of Chapter 7 of the Corporations Act and the entire Part 2 Div 2 of the ASIC Act, thereby reducing the number of places users need to look to find the law.

What would the FSL Schedule contain?

The FSL Schedule would contain the most important regulatory provisions, such as core obligations, core prohibitions, offence provisions, rights, remedies, and definitions.

The FSL Schedule would comprise three elements:

- all of the key financial services-related provisions that are currently found in Chapter 7 of the Corporations Act and Part 2 Div 2 of the ASIC Act; and

- objects clauses which would identify the fundamental norms of behaviour underpinning the legislation; and

- a list of defined terms.

The provisions of the FSL Schedule would be structured and framed in a way that would make it as easy to navigate and understand as possible. For more detail about how this could be done, see Chapter 5 of the Final Report.

Why did the ALRC recommend a schedule?

As discussed in Interim Report C, a schedule would allow the greatest flexibility to restructure and reframe the existing legislation while causing the least amount of disruption to other parts of the Corporations Act and ASIC Act.

In addition, the ALRC recommends that the Financial Services Law be contained in a schedule because:

- a schedule can be used to create a clearer legislative ‘identity’ for the regulation of financial services and to highlight common themes that traverse several chapters;

- it would be easier to facilitate integration of Part 2 Div 2 of the ASIC Act because all levels of the macrostructure (such as chapters and parts) could be used;

- retaining the substance of Chapter 7 in a schedule to the Corporations Act would enable existing linkages with other parts of the Act to be maintained more easily; and

- provision numbering in the schedule could ‘start afresh’, whereas any restructuring of the provisions of Chapter 7 of the Corporations Act would require renumbering.

What did stakeholders say about the idea?

A number of stakeholders provided submissions in response Interim Report C, where the ALRC first suggested the FSL Schedule. Stakeholders were generally supportive of the proposal.

Some stakeholders commented on the structure of the proposed FSL Schedule, and others made suggestions about other licensing regimes that could be included in the Schedule.

Several stakeholders expressed a preference for the Financial Services Law to be enacted as a standalone Act, but in light of existing constitutional constraints were supportive of the proposed schedule.

For further discussion, see the ALRC’s background paper on ‘Reflecting on Reforms III — Submissions to Interim Report C’.

Is there a risk that people will think the provisions in the FSL Schedule are less important than the provisions in the body of the Corporations Act?

This was a concern that some stakeholders raised with the ALRC. At least one stakeholder raised a concern that putting the Financial Services Law in a schedule ‘may lead to a perception that financial services regulation is not deserving of a prominent place in our Australian laws’.

However, the FSL Schedule would not be the first instance of a regulatory scheme being contained within a schedule to an Act. Other examples include:

- The Australian Consumer Law, in Sch 1 to the Competition and Consumer Act 2010 (Cth). The location of the Australian Consumer Law in a schedule was driven by the legislation’s constitutional basis, like the FSL Schedule.

- The Criminal Code in a schedule to the Criminal Code Act 1995 (Cth).

- The National Credit Code in which is Sch 1 to the National Consumer Credit Protection Act 2009 (Cth) (‘NCCP Act’).

- The Insolvency Practice Schedule (Corporations) and Insolvency Practice Schedule (Bankruptcy) contained in, respectively, Sch 2 to the Corporations Act and Sch 2 to the Bankruptcy Act 1966 (Cth).

As discussed in Interim Report C, experience with the Australian Consumer Law suggests that its location in a schedule has improved, rather than detracted from, public awareness of the legislation.

What alternatives did the ALRC consider?

During the Inquiry, the ALRC canvassed several alternatives, such as:

- enacting the Financial Services Law as a standalone Act;

- consolidating similar and overlapping regulatory regimes currently spread across different pieces of corporations and financial services legislation (for example, the Corporations Act, NCCP Act 2009 (Cth), ASIC Act, and Superannuation Industry (Supervision) Act 1993 (Cth)); and

- inserting the Financial Services Law as a new chapter within the Corporations Act.

For discussion of these alternatives, see Chapter 8 of the Final Report.

Why did the ALRC not recommend a standalone Act?

The ALRC has not recommended a standalone Act or consolidation of regulatory regimes for two main reasons. First, doing so may go beyond the Terms of Reference for the Inquiry, including because it may involve questions of policy.

Throughout the Inquiry, several stakeholders suggested there should be a standalone Act relating to financial services. In part, these suggestions stem from the perception that Chapter 7 of the Corporations Act is like an ‘Act within an Act’ in terms of its length and scope (see Chapter 8 of Interim Report C for further discussion). Some stakeholders would also prefer financial services provisions to be in a standalone Act to emphasise how important financial services regulation is within Australian law.

Second, enacting one or more standalone Acts would appear to be possible only by reforming the existing constitutional basis for the Corporations Act. In brief, the current referral of matters from the States to the Commonwealth would not empower the Commonwealth to enact other (standalone) primary legislation relating to the regulation of corporations and financial services.

Nevertheless, should a standalone Act or consolidation of regulatory regimes be considered, the ALRC’s recommendations could provide a useful starting point for that legislation.

For discussion of the constitutional underpinnings of the corporations and financial services legislation, see the ALRC’s background paper on ‘Historical Legislative Developments’ and Chapter 5 of the Final Report.

Why did the ALRC not recommend a new chapter of the Corporations Act?

The ALRC has not recommended that the Financial Services Law be enacted as a new chapter to the Corporations Act (or, alternatively, the ASIC Act) for two key reasons. First, there is no obvious ‘home’ for the Financial Services Law within either Act. Second, a schedule (as opposed to a new chapter) can be used to create a clearer legislative ‘identity’ for the regulation financial services and to highlight common themes that traverse several chapters.

Is it pronounced ‘shedule’ or ‘skedule’?

This question prompts heated debate on the internet (and even divides some of the ALRC team), so we’ll stay out of this one.

Throughout the Corporations and Financial Services Legislation Inquiry, stakeholders emphasised the importance of staging the implementation of reforms and managing transition costs. This article explains the ALRC’s suggested approach for implementing the reformed legislative framework for financial services.

This is the fourth in a series of short pieces following the release of the ALRC’s Final Report relating to the legislative framework for corporations and financial services regulation. In an earlier article, we outlined the reformed framework and explained how users would navigate it.

Why devote a whole chapter of the Final Report to Implementation?

Implementing reform comes with challenges and risks, such as transition costs and a risk that the job is left only half done. Chapter 7 of the Final Report details the ALRC’s approach to implementation and explains how the reformed legislative framework could be implemented in a logical, staged way so as to realise the benefits of reform as early as possible, minimise transition costs, and reduce the risk of it being left incomplete.

In summary, the ALRC’s suggested approach has two main elements:

- a Reform Roadmap (which sets out six Reform Pillars to guide implementation); and

- Steps to Implementation (which detail how each Reform Pillar should be approached).

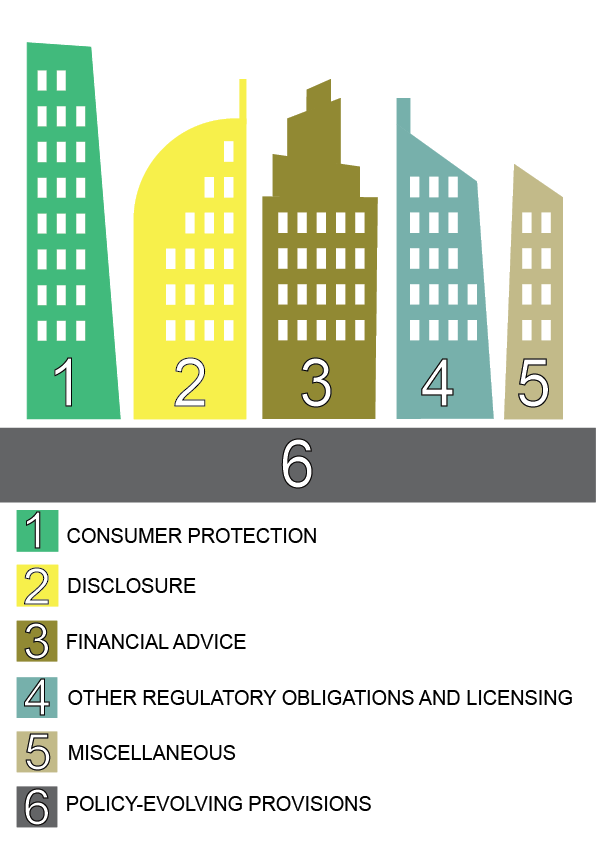

The Reform Roadmap and the Six Reform Pillars

The ALRC’s approach to implementing the reformed legislative framework is built on six Reform Pillars, shown in the following diagram:

The order of the Pillars is important. The Reform Roadmap is structured to realise the benefits of reform as early as possible.

- Pillar One (Consumer Protection) lays the foundation for future reforms. It does this by ensuring the legislation better communicates fundamental norms and frames the more specific obligations in later pillars.

- Pillar Two (Disclosure) would have a significant impact on reducing unnecessary complexity, with benefits for regulated persons, consumers, and investors.

- Pillar Three (Financial Advice) would bring together and consolidate the currently disparate provisions relating to financial advice, helping to reduce the costs of advice, support advisers to understand their obligations, and promote higher quality advice.

- Pillar Four (Other Regulatory Obligations and Licensing) would simplify the myriad regulatory obligations of financial services providers, and would complete the process of establishing a more navigable and comprehensible legislative framework.

- Pillar Five (Miscellaneous) would deal with reforms that are not captured by other pillars.

- Pillar Six (Policy-Evolving Provisions) provides a means of accommodating policy developments and policy reform alongside creation of the reformed legislative framework.

The ALRC recommends that the Reform Roadmap and implementation process be overseen by a specifically resourced taskforce (or taskforces) dedicated to that task (Recommendation 54). Taskforces are often used to implement reforms, drawing on expertise both within and outside government. Utilising a taskforce to implement reforms is an important way of minimising the challenges that confront any reform project.

Further detail about each of the Reform Pillars and taskforces is contained in Chapter 7 of the Final Report.

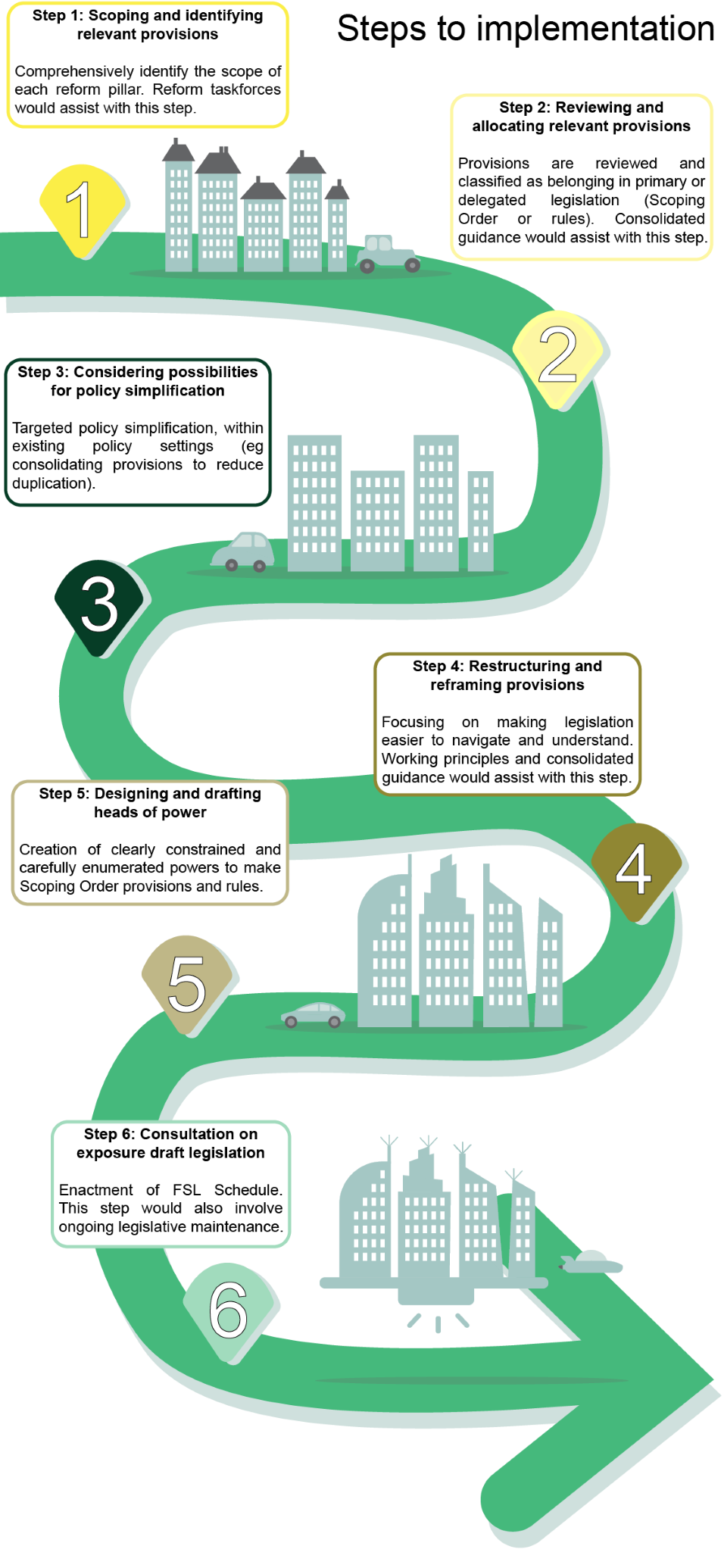

Steps to Implementation

Each Reform Pillar in the Roadmap would be implemented by following the six steps set out below:

In summary, the Steps to Implementation would involve:

- developing a clear understanding of the existing legislative framework and the design of the reformed legislative framework (Steps 1 and 2);

- looking at the bigger picture, to identify instances where targeted policy simplification could complement technical reforms to reduce legislative complexity (Step 3);

- applying best-practice principles of legislative design when preparing the legislation that implements the reformed legislative framework (Steps 4 and 5); and

- ensuring the reformed legislative framework is maintained into the future (Step 6), which should include periodic post-enactment review (Recommendation 55).

Chapter 7 of the Final Report contains further detail about the implementation process and explains the importance of ongoing legislative maintenance.

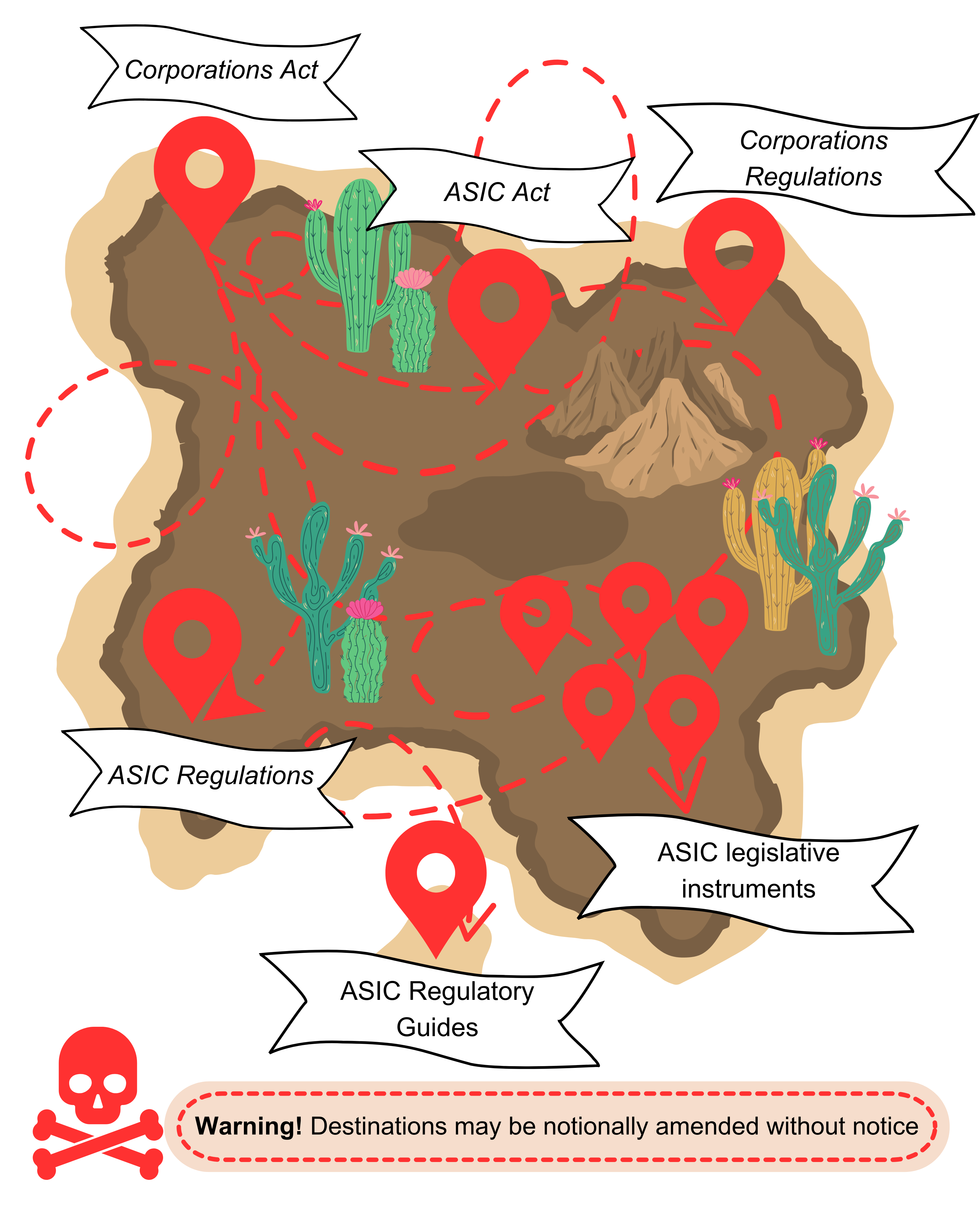

The ALRC used a number of analogies during the Corporations and Financial Services Legislation Inquiry to help explain our discoveries and conceptualise our insights about legislative complexity. We likened the law to a house, a cupboard, Russian dolls, and even outer space. Looking back, it often felt like we were on an archaeological dig, excavating layers of complexity when trying to understand the legislation we were meant to reform.

This infographic by ALRC Legal Officer/artist, Ellie Filkin, explores what that three-year archaeological dig looked like for the ALRC. It might resonate with some users of corporations and financial services legislation.

This is the third in a series of short pieces following the release of the ALRC’s Final Report relating to the legislative framework for corporations and financial services regulation.

The existing legislative framework for financial services is unnecessarily complex and difficult to use. So how should it be improved?

This article briefly explores the reformed legislative framework for financial services legislation recommended by the ALRC in the Final Report of the Corporations and Financial Services Legislation Inquiry. It also illustrates the benefits of the reformed legislative framework by showing how it would be much simpler to navigate than the existing legislative framework.

This is the second article in a series of short pieces following the release of the ALRC’s Final Report. Revisit the first article here.

The existing legislative framework

Currently, if a person wants to use financial services legislation, they must wade their way through voluminous Acts, regulations, legislative instruments, and guides, with little indication as to what they can expect to find and where. Navigating the existing legislative framework is a bit like using a treasure map that has many paths, but no clear destination:

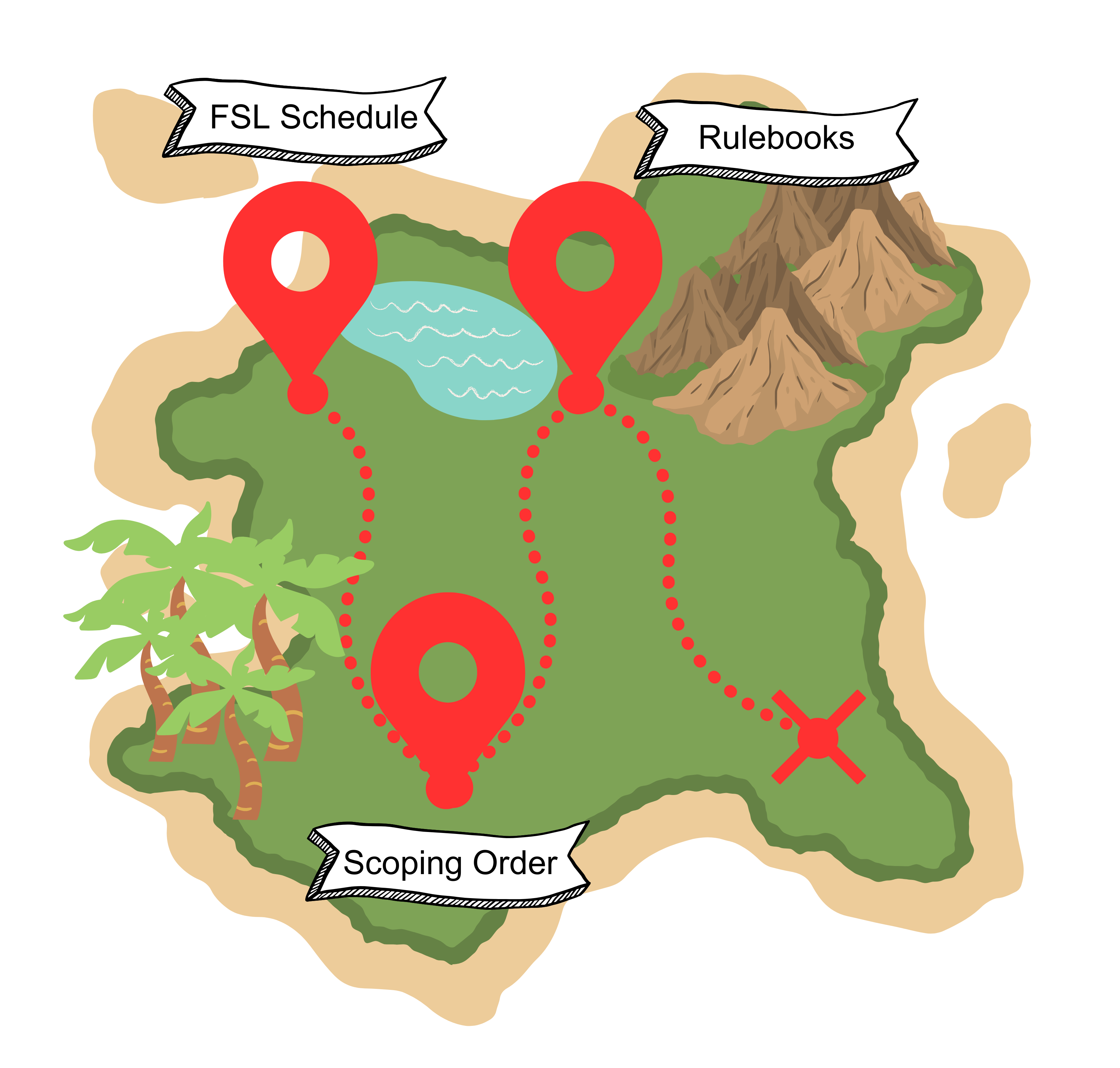

The reformed legislative framework

If implemented, the ALRC’s recommendations would transform the existing legislative framework into the reformed legislative framework.

The reformed legislative framework is intended to be clear, user-friendly, and easy to navigate:

- Users would start with the Financial Services Law Schedule (‘FSL Schedule’), where they would find key provisions including important obligations, prohibitions, offences, and penalties. The FSL Schedule would be enacted by Parliament, reflecting the significance of its contents.

- Users would then move to the single, consolidated Scoping Order. In the Scoping Order, users would find provisions that set the scope of the regulatory framework, such as exclusions.

- Users would then move to thematic Rulebooks, where they would find prescriptive detail about how to comply with obligations in the FSL Schedule.

Compared to the existing legislative framework, users would end their journey (where ‘x’ marks the spot) having followed a clearly defined path and without the need to consider whether any part of the law has been notionally amended by another piece legislation. Because the reformed legislative framework would be simple to navigate, it would also be easier for users to develop a clear understanding of their obligations or rights.

Each element of the reformed legislative framework is based on working principles for legislative design set out in the Final Report, all of which help to make the framework easier to navigate and understand:

Each element of the reformed legislative framework is based on working principles for legislative design set out in the Final Report, all of which help to make the framework easier to navigate and understand:

- coherence;

- grouping thematically related provisions;

- intuitive flow;

- prioritisation;

- succinctness;

- consolidating similar provisions; and

- mental models.

Though directed at the legislation that governs financial services, the principles that underpin the reformed legislative framework could be applied to other legislation (especially complex legislation).

For more information, see the Final Report:

- Chapter 3 gives an overview of the reformed legislative framework;

- Chapter 4 discusses the ALRC’s working principles for legislative design that underpin the reformed legislative framework; and

- Chapters 5 and 6 set out the elements of the reformed legislative framework in more detail, discussing how the primary legislation should be restructured and reframed (Chapter 5) and make better use of the legislative hierarchy (Chapter 6).

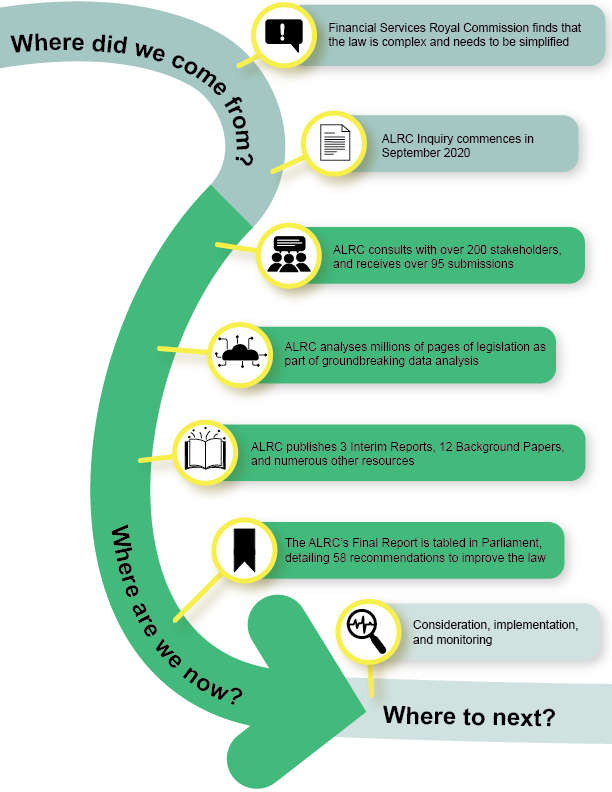

Last week, the Final Report of the ALRC’s Corporations and Financial Services Inquiry was published. The Final Report laid out the results of three years’ work examining why the law is so complex and setting out how it should be reformed. In this article, we describe the ALRC’s journey from the Inquiry’s genesis through to next steps.

This is the first in a series of short articles following the release of the Final Report. Each piece aims to give a simple overview of the ALRC’s recommendations and important themes from the inquiry.

Where did we come from?

In 2019, the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (also known as the Hayne Royal Commission) found that corporations and financial services legislation is overly complex and in need of simplification. In particular, the Royal Commission found that financial services legislation fails to communicate the fundamental norms of behaviour that it promotes.

Against this background, the Australian Government gave the ALRC Terms of Reference, which tasked the ALRC with making financial services and corporations legislation clearer and more understandable.

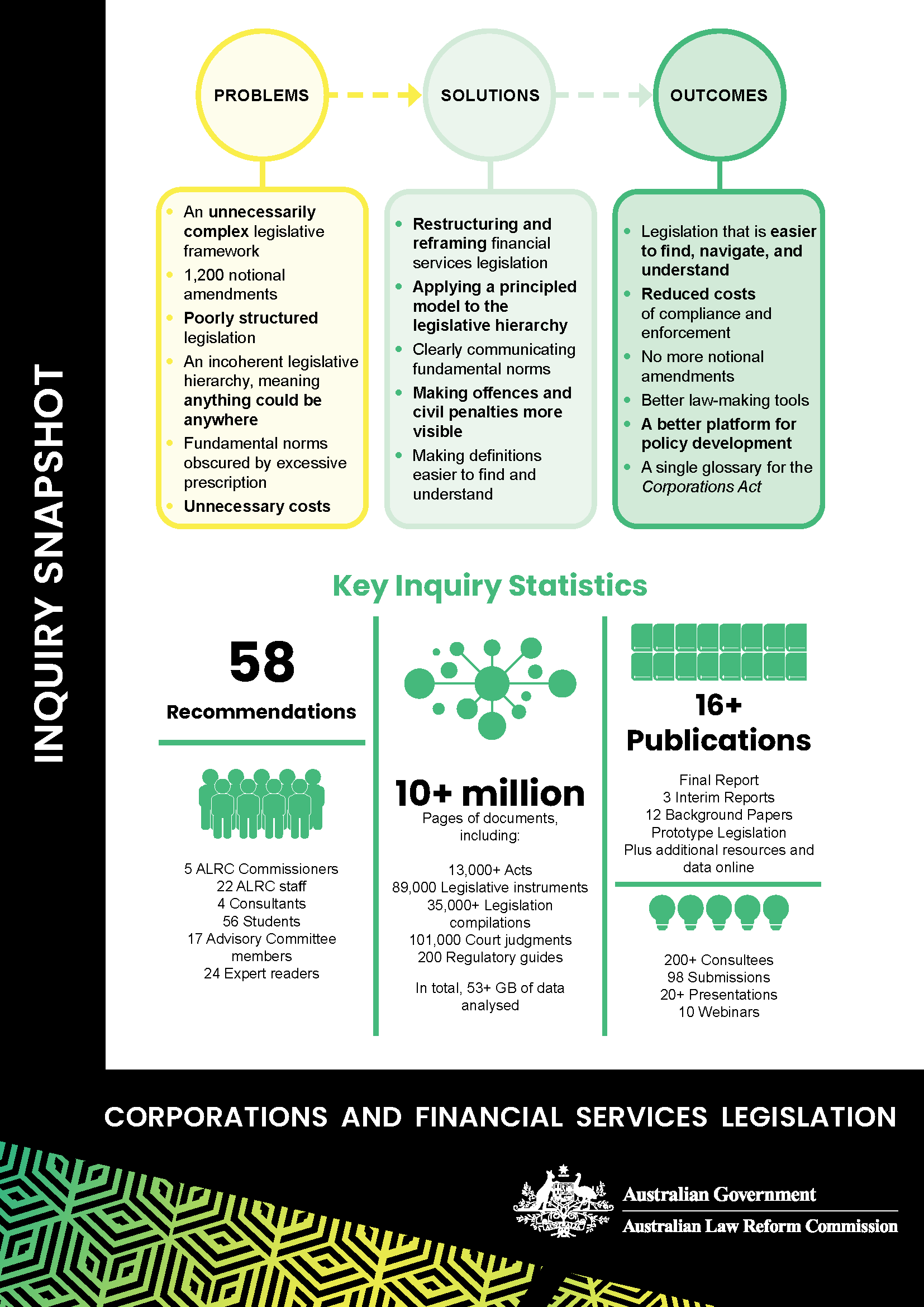

The ALRC’s analysis confirms that corporations and financial services legislation remains unnecessarily complex. The main sources of unnecessary complexity include:

- an incoherent legislative hierarchy;

- poorly designed primary and delegated legislation;

- issues with law-making processes and legislative maintenance;

- extensive use of notional amendments; and

- proliferating powers and instruments creating a legislative maze.

See Chapter 2 of the Final Report for more details.

Where are we now?

The ALRC consulted with a wide variety of stakeholders, including regulators, government departments, academics, legal professionals, and industry representative bodies. Stakeholders were given the opportunity to provide feedback and formal submissions in response to the ALRC’s preliminary proposals throughout the Inquiry. Stakeholders almost universally agreed with the ALRC that the existing legislation is complex and that it should be simplified.

The ALRC also produced groundbreaking new empirical data analysis, providing fresh insights into the causes and consequences of legislative complexity. The ALRC’s empirical analysis confirmed stakeholders’ anecdotal experience of complexity. Further detail about the ALRC’s data analysis is available on the ALRC Data Hub.

Throughout the Inquiry, the ALRC published 12 Background Papers, and three Interim Reports.

The ALRC has now published its Final Report, which contains 58 recommendations for reform (23 of these recommendations were made in the three Interim Reports). These recommendations aim to simplify and rationalise corporations and financial services legislation, making it easier to use and understand.

Where to next?

Now that the Final Report has been published, the Australian Government will consider which of the ALRC’s recommendations should be implemented. Several recommendations made by the ALRC in Interim Reports A and B have already been implemented.

Chapter 7 of the Final Report sets out a staged process for implementing many of the recommendations. This staged process categorises the recommendations into six ‘Pillars’. See Chapter 7 of the Final Report for more details.

The ALRC has also recommended several measures to ensure that the recommendations have an enduring effect into the future. This includes the creation of guidance for legislative drafting, and a legislative data framework to monitor the development of corporations and financial services legislation.

The Australian Law Reform Commission Final Report, Confronting Complexity: Reforming Corporations and Financial Services Legislation (Report 141, 2023), was tabled in Parliament today by the Attorney-General, the Hon Mark Dreyfus KC MP.

The report found that the legislation governing Australia’s financial services industry is a tangled mess — difficult to navigate, costly to comply with, and unnecessarily difficult to enforce.

Judges have described the current laws as being like ‘porridge’, ‘tortuous’, ‘treacherous’, and ‘labyrinthine’. Others have described the legislation as ‘broken’. Complexity in the existing legislation is not an isolated problem — it costs businesses, consumers, investors, and the economy at large. The ALRC has made 58 recommendations to simplify the law, including a revamped legislative framework for the financial services sector. These reforms aim to reduce costs for service providers and consumers, improve productivity by reducing complexity, and provide clarity around compliance requirements and enforcement. Thirteen recommendations made during the Inquiry have already been implemented, in full or in part, by legislation passed during 2023.

Recommendations in the Final Report include:

- Redesigning financial services legislation to give it a clear home and identity as the ‘Financial Services Law,’ making it easier and less costly to find, navigate, and understand.

- Ending the use of almost invisible notional amendments that make the law deeply inaccessible, and instead using thematic, consolidated rulebooks to provide flexibility for regulating particular products, persons, services, or circumstances.

- Making it easier to tell when something is a ‘financial product’ or ‘financial service’ by introducing a single, simplified definition of both terms.

- Making offence and penalty provisions less complex and more obvious by consolidating them into a smaller number of provisions that cover the same conduct, making them easier to identify, and making the consequences of breach clear on the face of the law.

The report follows on from the findings of the Royal Commission into Misconduct in the Banking, Superannuation, and Financial Services Industry in 2019 that exposed the deficiencies of the current legal infrastructure.

Complexity costs consumers not only in the expenses that are passed on by financial services providers, but by failing to protect them from misconduct. The Royal Commission clearly demonstrated the economic and human costs of non-compliance with the law. The ALRC’s reforms would strengthen consumer protection substantially and reduce costs for business by making the law simpler to comply with and easier to enforce.

QUOTES — Justice Mordy Bromberg, President of the ALRC

‘Australia’s laws governing financial services are a confusing maze and need to be overhauled. The reforms outlined in this report will make these laws easier to understand and navigate, drive down the costs associated with complying with the law, and make it easier for consumers to understand and enforce their rights.’

‘These laws provide the legal and economic infrastructure of the financial services industry. The reforms we’re proposing are broadly supported by stakeholders and if implemented will see substantial improvements for both consumers and business.’

ENDS

Download the Final Report

Download the Summary Report

About the Australian Law Reform Commission

The Australian Law Reform Commission (ALRC) is an independent Australian Government agency that provides recommendations for law reform to Government on issues referred to it by the Attorney-General of Australia.

|

|

|

|

|

|

|

Media contact: |

Francis Leach, Media and Communications Director comms@alrc.gov.au, 0409 947 180 |

Author: Dr Vannessa Ho

As the ALRC’s Financial Services Legislation Inquiry reaches its conclusion, it pays to look to the future. In an ever-evolving technological landscape, what will be the next challenge for financial services law? This article explores some recent innovations and the regulatory challenges they (and similar future developments) pose in the context of financial services law.

Continually evolving technologies

Technological advancements can lead to new or more efficient business practices in the financial services industry. However, the law can struggle to keep up with the fast pace of technological progress. This challenge is not new, and technology will continue to evolve in unanticipated ways. The question then becomes, how can financial services legislation be reformed to best accommodate continually evolving technologies?

The Australian Government has recognised the need to modernise financial services regulation. The ALRC’s forthcoming Final Report for the Financial Services Legislation Inquiry (‘Final Report’) seeks to outline reform that would produce a more adaptive legislative framework. Adaptivity in the face of technological development can help to support innovation and protect consumers from harm, thereby helping to ensure that markets for financial services operate efficiently and productively.

The regulatory challenges of evolving technologies

While financial services legislation should be technology neutral, challenges when regulating evolving technology persist. This is partly because it is difficult to determine how, and whether, legislation should regulate new technologies. There are also competing interests which may need to be considered before extending existing legislation to uses of new technology. For example, the law aims to protect consumers without imposing burdensome regulation that has the effect of stifling innovation. Three examples highlight the regulatory challenges of new technology: automated financial advice (commonly known as ‘robo-advice’); buy now pay later (‘BNPL’); and crypto assets.

Robo-advice

The term ‘robo-advice’ is used to encompass a wide range of technological capabilities. ASIC defines the term expansively to include ‘the provision of automated financial product advice using algorithms and technology without direct involvement of a human adviser’. Robo-advice can be used to provide financial advice on superannuation, other investments, mortgages, insurance, and credit products (see Ringe and Ruof’s article for further discussion on the current capabilities of robo-advice).

Robo-advice has the potential to benefit consumers as it could make financial product advice more affordable and convenient. This, in turn, could encourage more consumers to seek out financial advice before making important financial decisions. Further, with continual advancements in artificial intelligence, robo-advice seems likely to become more sophisticated, which may reduce the amount of human intervention needed when providing automated advice.

The existing legislative framework for financial services in Australia applies to robo-advice in the same way that it applies to human advice. This means that any weaknesses in the existing legislative framework would also affect robo-advice. Throughout the Financial Services Legislation Inquiry, the ALRC has highlighted how financial services legislation is unnecessarily complex. The legislative framework contains excessive prescriptive detail, is difficult to navigate, and costly to comply with. This complexity is likely to be a deterrent for firms that have the technological capability to enter the robo-advice sector.

There are many ways the existing legislative framework could be reformed to accommodate robo-advice. This article discusses the regulatory challenges associated with two options.

The first option would be to create bespoke legislation for robo-advice. The main challenge with this approach, however, is that robo-advice is still an emerging technology. The risks of a bespoke legislative framework for any emerging technology include:

- ensuring legislation is drafted to be sufficiently technology neutral, so that it does not become redundant as the technology evolves;

- if the legislative framework is restrictive or produces uncertainty, it may disincentivise firms looking to invest in research and development of the technology; and

- if legislation is too prescriptive, it is likely to require tailoring, exemptions, and carve-outs as the technology evolves.

The ALRC’s Inquiry has shown how excessive prescription and incoherent use of the legislative hierarchy to tailor regulatory regimes is a significant source of complexity. A more coherent approach to using the legislative hierarchy, such as that discussed in Interim Report B, would help to minimise this complexity.

The second option would be to maintain the current approach and continue to treat robo-advice in the same way as human financial advice. Under this option, reform could be made to the existing financial product advice regime. For example, the Quality of Advice Review discussed ‘digital advice’, which includes (and is sometimes used synonymously with) robo-advice. The Quality of Advice Review concluded that its recommendations would help facilitate digital advice. The Australian Government is now consulting further on the recommendations made by the Quality of Advice Review and potential changes to financial advice provisions in the Corporations Act 2001 (Cth) (‘Corporations Act’).

Changes to financial advice provisions may be further supported by the ALRC’s reforms which aim to improve navigability and increase the adaptivity of the financial services legislative framework. A more navigable and adaptive legislative framework would facilitate the advancement of robo-advice technologies, and similar innovations, by making the legislation less costly to comply with.

Buy now pay later

ASIC describes BNPL as an arrangement that ‘allow consumers to buy and receive goods and services immediately from a merchant, and repay a [BNPL] provider over time’. Specific BNPL arrangements may vary depending upon what features the provider offers. However, consumers may seek to use BNPL because:

- it enables them to delay payment but obtain goods and services immediately;

- interest is generally not charged; and

- it can be easier to set up than a credit card or personal loan.

Many BNPL arrangements can fall outside the existing regulatory framework for financial services and credit. As a result, there are increasing concerns that BNPL may cause consumer harms, such as financial stress, hardship, and excessive fees. In response to these concerns and due to the similarity of BNPL with traditional credit facilities, the Australian Government has committed to extending the National Consumer Credit Protection Act 2009 (Cth) (‘NCCP Act’) so that it captures BNPL arrangements. However, due to the variety of BNPL arrangements, there may be challenges when extending the existing credit regime. These challenges are likely to include:

- defining the concept of BNPL to ensure it encompasses a sufficiently broad range of business models;

- tailoring the responsible lending requirements of the NCCP Act to protect consumers without stifling innovation; and

- preventing unnecessary legislative complexity from creeping further into the credit regime, with the aim of avoiding the level of complexity that has developed within the Corporations Act.

Crypto assets

As highlighted in the ALRC’s Background Paper ‘New Business Models, Technologies, and Practices’, crypto assets can be defined in different ways and for different purposes. Crypto assets have also been variously referred to as digital assets, virtual assets, tokens, or coins. One description of crypto assets, advanced by Treasury, is that it

is a digital representation of value that can be transferred, stored, or traded electronically. Crypto assets use cryptography and distributed ledger technology.

Treasury has more recently undertaken a token mapping exercise to examine the crypto ecosystem within Australia and its intersection with existing financial services legislation. The token mapping exercise developed an understanding of the key concepts of crypto assets and related terms like crypto networks, tokens, and token systems. This exercise is a step towards policy development for the regulation of crypto assets within Australia.

The existing definitions of ‘financial product’ in Australian legislation are framed in technology neutral terms. This means that crypto assets are capable of meeting these definitions and falling within the existing regulatory regime. Regulatory challenges largely stem from the wide variety of crypto assets and the subsequent difficulty in reaching a settled definition. The obstacles caused by developing a coherent definition of crypto assets may be somewhat resolved by Treasury’s token mapping exercise. However, Treasury has noted that some types of token systems may not fit within the existing framework.

Following the token mapping exercise, Treasury released a consultation paper on a proposal which seeks to ‘introduce a regulatory framework to address consumer harms in the crypto ecosystem while supporting innovation’. Rather than regulate crypto assets directly, Treasury proposes to regulate crypto exchanges via the Australian Financial Services licensing regime, thereby requiring crypto exchanges to meet a licensee’s obligations and requirements within the Corporations Act. Regardless of the form this proposal takes, it is still important that the legislative framework be adaptive to support innovation of the crypto economy.

What could be done?

The regulatory challenges of evolving technologies highlight the importance of an adaptive, efficient, and navigable legislative framework. This is the case for technologies that fall within the existing legislative framework (such as robo-advice) and technologies for which policy is being developed (such as BNPL and crypto assets). The findings of the ALRC’s Inquiry demonstrate that the existing legislative framework for financial services is unnecessarily complex — it is difficult to navigate, hard to understand, and key principles are often buried in prescriptive detail. Adaptation in the existing legislative framework often takes the form of complex notional amendments and conditional exemptions, spread incoherently across the legislative hierarchy. This increases the costs of compliance and creates barriers to innovation.

The ALRC’s Final Report will contain recommendations aimed at reforming the existing legislative framework so that it is more adaptive, efficient, and navigable. The ALRC’s recommendations will focus on:

- restructuring and reframing financial services legislation to better communicate its core requirements and emphasise fundamental norms of behaviour;

- creating more coherent and principled use of the legislative hierarchy, making the legislative framework easier to navigate and more adaptive (without generating unnecessary complexity); and

- ensuring definitions are easier to find and understand.

Conclusion

The are many benefits of using evolving technology to innovate and enhance productivity. Tempered against these benefits, however, is a need for sufficient consumer protection where there is risk of significant harm. The ALRC’s forthcoming Final Report will discuss how the existing legislative framework for financial services legislation is unnecessarily complex. In the context of evolving technology, this complexity can stifle innovation and productivity, and undermine consumer protection. Complexity in the existing legislative framework also makes it harder to implement policy initiatives aimed at regulating emerging technologies. The reforms recommended by the ALRC in the Final Report aim to produce an adaptive legislative framework for financial services that can support innovation, policy development, and consumer protection more effectively than at present.

Author: Jane Hall

Emojis are ubiquitous in modern communication. In 2021, Unicode reported that 92% of the world’s online population use emojis. Emojipedia estimates that over 900 million emojis are sent each day without text on Facebook Messenger, and that by mid-2015, half of all comments on Instagram included an emoji.

Given how frequently we use emojis, it should come as no surprise that emojis are making their way into the law (a recent episode of the Law Report on Radio National explored this development). A recent decision of the King’s Bench for Saskatchewan made headlines when the court determined that the 👍 emoji could be a legally binding indication of agreement to a contract (see South West Terminal Ltd v Achter Land & Cattle Ltd [2023] SKKB 116). This decision was one in a growing line of cases where courts have been asked to interpret the meaning and legal effect of different emojis (see Eric Goldman, ‘Emojis and the Law’).

This article explores another potential use for emojis: legislative drafting. The ALRC is currently preparing its Final Report in the Financial Services Legislation Inquiry. Throughout the Inquiry, the ALRC has explored ways to improve the navigability and comprehensibility of legislation. If emojis are already cemented in our daily lives, could they also help make legislation easier to navigate and understand?

After examining how the law has started to use emojis and other images, this article considers:

- 🥸 the characteristics of good legislation and the goals of legislative design;

- 🎨 how emojis could be used in legislation; and

- 🏆 whether emojis could help achieve the goals of good legislative design.

While emojis may improve the navigability and comprehensibility of legislation, these benefits are (for the foreseeable future at least) likely to be outweighed by the additional uncertainty 🫤 and ambiguity 🙃 emojis introduce.

🤔 Why consider using emojis in legislation?

Emojis are not just playful devices to express our sense of humour, or to send subliminal messages. They can have serious legal consequences.

For example, in In re Bed Bath & Beyond Corp. Securities Litigation, 2023 U.S. Dist. LEXIS 129613 (D.D.C. July 27, 2023), the US District Court found that the use of the ‘full moon face’ emoji (🌝), in a Tweet by the respondent, Cohen, about shares in a particular company could be understood by shareholders as an indication that the stock would increase in value and that shareholders should therefore buy or hold stocks. The Court stated:

In the meme stock “subculture,” moon emojis are associated with the phrase “to the moon,” which investors use to indicate “that a stock will rise.” So meme stock investors conceivably understood Cohen’s tweet to mean that Cohen was confident in Bed Bath and that he was encouraging them to act.

In South West Terminal, the Court determined that the 👍 emoji could act as a signature on a contract for the delivery of flax. The court recognised that the use of the 👍 emoji was a ‘non-traditional’ means of signing a contract but that nonetheless, in circumstances where the parties had previously reached similar agreements via text message, it was a valid way to convey the purposes of a signature.

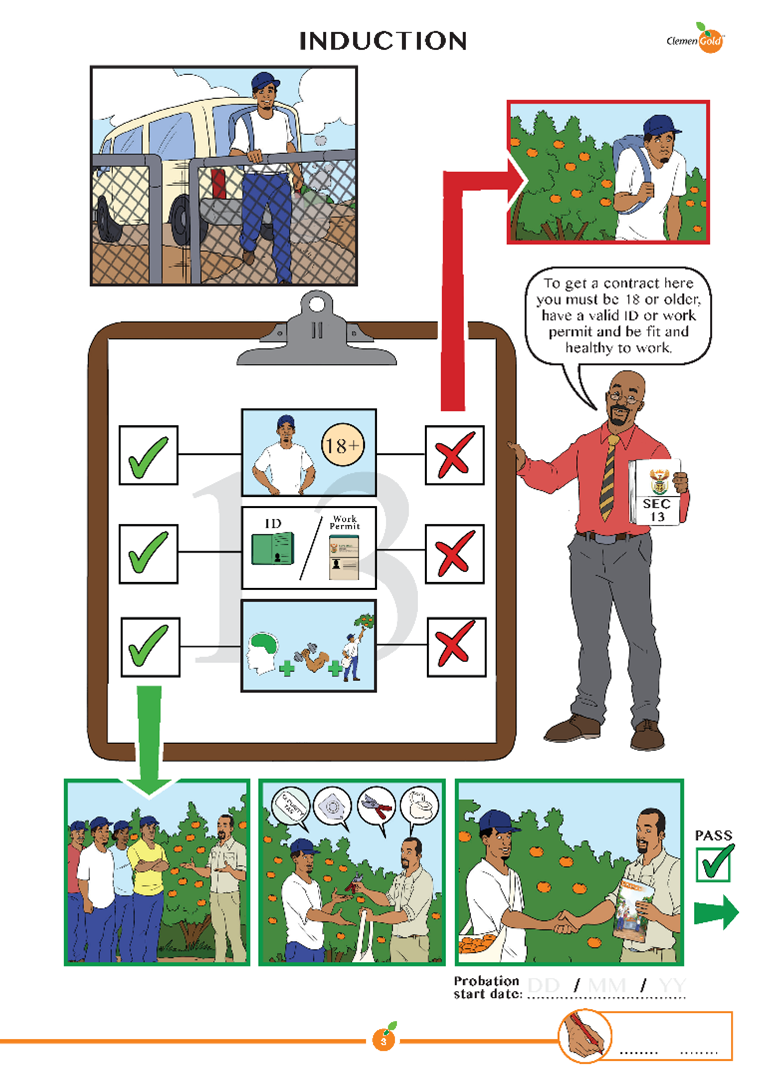

These cases can be seen as part of a broader trend of embracing images to affect legal interactions and to make the law more accessible. Initiatives such as Comic Book Contracts and Creative Contracts have been exploring the use of visual and cartoon-based contracts. Cartoon-based contracts use images to convey the key terms of the contract. Sometimes the images are accompanied by simplified text but other times the contract only contains images. These types of contracts have been particularly useful for linguistically diverse workplaces. For example, Creative Contracts developed an employment contract for a citrus farming business in South Africa, a country in which multiple languages are spoken. The cartoon-based contracts produced by Creative Contracts ‘reduced the induction time from four hours to 40 minutes’, reflecting the potential for images to effectively convey information.

Source: Creative Contracts (https://creative-contracts.com/clemengold/)

In 2018, Aurecon and the University of Western Australia co-designed the first employment contract for an Australian workplace that combined text and images to make concepts like probation and leave entitlements more easily comprehensible to a workforce that did not have legal training.

Legislative drafters too have been experimenting with different ways of presenting information to improve the ‘readability’ of legislation. For example, guidance from the Office of the Parliamentary Counsel emphasises the use of ‘readability aids’, which includes the use of visual aids such as flow-charts (see, eg, Evidence Act 1995 (Cth) ch 3, which uses a flowchart to show how the Chapter applies to particular evidence).

If we are already using emojis in ways that affect legal relations and to develop contracts, and we’re already experimenting with different readability aids, it begs the question: is the next logical step to use emojis in legislation? Could emojis help to make legislation more accessible?

🥸 What does good legislation look like?

The question ‘what makes for good legislation’ will be answered differently depending on who you ask. In this article, I assess the quality of legislation by reference to how easy it is to access and use.

The ALRC has previously published on good legislative design and user-friendly legislation, and has proposed seven working principles for the structuring and framing of corporations and financial services legislation in Interim Report C. This article focuses on the concept of ‘mental models’ that enhance the navigability and comprehensibility of legislation. I consider that good mental models focus on the following:

- 👌 simplicity (improving the coherence and clarity of the legislation);

- 💡 comprehensibility (highlighting important matters that may not be immediately apparent); and

- 🧭 navigability (both within and between Acts).

These three elements will form the criteria for assessing the potential effectiveness of emojis in legislative design.

🎨 How could emojis be used in legislative drafting?

Using emojis in legislative drafting does not mean turning legislation into a visual cryptic crossword by replacing all references to ‘Australia’ with the 🦘 or 🐨 emoji, or substituting the 🧑⚖️ emoji for the word ‘court’. Rather, emojis could be used as visual aids, or signalling devices, to improve the navigability of legislation by:

- ❗ highlighting important matters, such as offence provisions;

- 🔎 identifying matters that may not be immediately apparent on the face of the provision, such as defined terms or notional amendments; and

- 👩🎨 improving the visual appeal of legislation.

🧪 Case study: section 791A of the Corporations Act 2001 (Cth)

To illustrate what this could look like, I took a current provision from the Corporations Act 2001 (Cth) and inserted emoji ‘signals’. The provision is currently located in Chapter 7 of the Corporations Act, a chapter described as being like an old cupboard in need of a good spring clean 🧹.

The provision currently reads:

Emojis could be used as signalling devices to highlight the following:

|

Information |

Emoji |

|

Section 791A is a civil penalty provision |

🚫 |

|

Sub-section (1) contains an obligation |

⚠️ |

|

The provision contains terms that are defined in the Corporations Act 2001 (Cth) |

📖 |

|

The provision contains terms that are defined in other legislation |

📘 |

|

The provision was introduced after the Corporations Act 2001 (Cth) was enacted and has been subsequently amended |

📝 |

The reframed provision could look like the following:

Does it work?

The reframed provision appears to partially satisfy the criteria for a good mental model:

|

|

Aim |

Achieved? |

|

|

Simplicity |

Coherence and clarity |

🤔 |

While the emojis are useful signalling devices, they remove some whitespace and may make the provision seem crowded. There is a risk of ‘information overload’. |

|

Comprehensibility |

Highlight important matters that may not be apparent on the face of the legislation |

✅ |

The emojis highlight that the provision contains obligations and offence provisions, and that it has been amended since its enactment. |

|

Navigability |

Improve navigability within the Act and with other Acts |

🤔 |

The emojis identify terms that are defined within this Act, and tell users that certain terms are defined in other Acts. But, the emojis are quite distracting, an issue the ALRC has previously noted when it comes to identifying defined terms. |

👎 The downsides

While there is certainly a case for using emojis to assist with the simplicity, comprehensibility, and navigability of legislation, embracing emojis in legislation comes with some potential downsides. Goldman identifies five key issues with the use of emojis in law more generally:

- 🕵️ visual decoding (emojis are relatively small in size and several emojis look quite similar, which can make it difficult to identify which emoji has been used);

- 👯♀️ multiple meanings (there is no definitive reference source catalogue for emojis and Unicode’s criteria for accepting new emojis suggests that it prefers emojis that have multiple potential uses);

- 😵💫 depiction diversity (emojis appear differently on different platforms, which can increase confusion as to their intended meaning);

- 💂♀️ culture-specific meanings, which inform metonyms (using emojis as a form of figurative language to replace words or expressions, such as using the 🤔 emoji instead of the phrase ‘hmm’ or ‘let me think’ – see Javier Morras and Antonio Barcelona, ‘Emojis: Metonymy in Meaning and Use’); and

- 🖊️ unsettled grammatical rules when using multiple emojis in a thread.

The first three of these issues are particularly relevant for emojis in legislation.

Visual decoding may undermine the potential for emojis to be useful signalling devices in legislation. If it is difficult to identify which emoji has been used, then readers will not benefit from the visual prompt.

For example, the 📝 emoji (which in the example above indicates that the provision has been amended since the statute’s enactment) could be confused with another writing-based emoji, such as: 📃📄📜🗒️. At best, this may result in users of legislation simply ignoring the emoji. At worst, it could result in confusion and uncertainty.

Multiple meanings could create ambiguity and uncertainty.

For example, while in South West Terminal the 👍emoji was interpreted as a signature on a contract, in Lightstone RE LLC v Zinntex LLC, 2022 N.Y. Misc. LEXIS 5925 (N.Y. Supreme Ct. Aug. 25, 2022), the Supreme Court of New York considered that the same emoji did not constitute acceptance of a contract in circumstances where the surrounding text messages showed that the sender did not intend to be bound by the agreement. Even in South West Terminal there was argument about whether the 👍emoji should merely be interpreted as a confirmation of receipt of the text message.

Such ambiguity could be mitigated through an interpretive provision being inserted into the Acts Interpretation Act 1901 (Cth) to explain what the emojis indicate. Such a provision could be along the lines of:

Use of emojis

If a provision of an Act includes an emoji, the following table provides the meaning of the emoji in the particular context.

|

References to Emojis in Acts |

|||

|

Item |

If the provision uses the following emoji |

in the following context |

then the emoji indicates … |

|

1 |

📝 |

in the margin next to a provision title |

that the provision has been amended since enactment |

|

2 |

📖 |

in the margin of a provision followed by certain terms |

that those terms are defined terms within the Act |

|

3 |

📘 |

in the margin of a provision followed by certain terms |

that those terms have a defined meaning in another Act, which applies to this Act |

|

4 |

⚠️ |

in the margin of a sub-provision |

that the sub-provision contains an obligation |

|

5 |

🚫 |

in the margin of a sub-provision |

that the sub-provision is an offence provision |

However, it may be unrealistic to expect that users of legislation would instinctively turn to the Acts Interpretation Act to resolve any confusion they have as to the meaning of an emoji that appears in an Act. It is more likely that users would rely on their own understanding of the emoji, which could differ significantly from another user’s understanding, or would run a search on the internet to learn the meaning. This would lead to further issues because legislation would be giving the emoji a new, context-specific meaning that may differ from what users would understand to be the ‘ordinary meaning’ of the emoji.

Another option would be to use ‘hover boxes’ to show the intended meaning of the emoji. However, this may be limited by the current capabilities of the Federal Register of Legislation.

Depiction diversity would likely cause issues because users of legislation may not recognise the emoji if its depiction in legislation differs from the way that the emoji appears on a user’s platform.

For example, the ‘full moon face’ emoji referred to in South West Terminal is depicted quite differently on various platforms:

|

Apple |

Microsoft |

|

Noto Emoji Font |

|

Twitter/X |

|

|

|

|

|

|

If we are going to use emojis in legislation, we may need to accept that the depiction that is chosen is likely to be recognisable to people familiar with that platform but may be unrecognisable or confusing for people familiar with a different platform, or who do not use emojis at all. The ability of users to recognise the emoji, and to understand its meaning, would therefore depend on (a) whether that person uses emojis at all, and (b) which platform the user is most familiar with. This would seem to undermine the purpose of using emojis: to increase the accessibility and navigability of legislation. It is also at odds with the principle that legislation should be generally accessible and comprehensible by all users.

The combined effect of these three issues is to produce a level of ambiguity and legal uncertainty that seems to outweigh the benefits emojis could bring to legislation.

💭 Conclusion

Parts of the Commonwealth statute book are in need of an upgrade and an update. The ALRC is currently reviewing financial services legislation in an attempt to make it easier to navigate and understand. The question is, could emojis help achieve those aims? 🤔

In the case of financial services legislation, any improvement to navigability and comprehensibility would seem to be outweighed by the increased ambiguity and uncertainty that emojis would introduce😞 .

While emojis may not be the solution for reforming financial services legislation, there could be a case for using emojis as legislative signalling devices to help bring legislation into the twenty-first century 🪄 . I commend anyone brave enough to attempt that feat 👏 .